Senior Consultant, Voluntary Emissions

Highwood Emissions Management

Differentiated Gas Technologist

Highwood Emissions Management

Emissions Engineer-In-Training

Highwood Emissions Management

Chief Executive Officer

Highwood Emissions Management

Vice President Consulting

Highwood Emissions Management

President & Chief Innovation Officer

Highwood Emissions Management

Director, Research & Development

Highwood Emissions Management

As we launch the third edition of our annual Voluntary Initiatives report, I am filled at once with wonder and gratitude. Wonder at how far our industry has come in only three years, in terms of our collective emissions knowledge, competencies, and sustained commitment to progress. Gratitude for those who have done the work to get us here – including industry, regulators, academics, non-profits, service providers, innovators, and educators. Many of the visionaries pushing our industry forward are the same individuals and organizations who have made this report possible. We extend our sincere thanks to our sponsors for funding this report, to the administering organizations for their cooperation and contributions, to our colleagues and mentors for their guidance, and to the Highwood team – especially those who have worked tirelessly for months to produce this report. We look forward to another year of hard work – alongside all of you – in our mission to deliver cleaner and more affordable energy.

President & Chief Innovation Officer

Highwood Emissions Management

Global demand for energy continues to increase, alongside energy transition pressure. With a rising global demand for sustainable and affordable energy, operators in the oil and gas industry are looking for strategies to balance or reduce the greenhouse gas (GHG) emissions footprint from their operations. As a large global emitter, the oil and gas industry is expected to contribute to GHG emission reductions to meet the goals set by the 2015 Paris Agreement.

Energy transition is often misunderstood. Throughout history, transitions have occurred due to technological developments, or scarcity of existing resources. Today’s energy transition factors in environmental concerns and the need to mitigate climate change. However, transition is not about a hard-stop on existing energy sources, but rather a collaborative approach to lowering the carbon footprint of existing supply in conjunction with the development of new low-carbon solutions.

The energy industry will be part of the solution. Minimizing and managing emissions from oil and gas production is not only becoming a regulatory requirement, but also a benchmark for stakeholders to evaluate and grant social license. By taking a proactive approach to emissions management and going beyond the minimum regulatory requirements, energy companies can differentiate themselves to Environmental, Social, and Governance (ESG) conscious stakeholders, profit from reduced leakage, as well as benefit from premiums for certified low-carbon products.

Voluntary Initiatives are an essential part of the solution. Early in 2021, our team at Highwood Emissions Management (Highwood) observed a rapidly growing ecosystem of voluntary initiatives available to the energy industry. Our clients expressed increasing confusion as they attempted to navigate a new and expanding network of programs, asking questions like “Which one is best?” and “What is the benefit to my organization?”.

Our first report in 2021 broke new ground. It brought structure and guidance to the rapidly emerging voluntary initiatives landscape. We identified 20 distinct voluntary initiatives and categorized them as certifications, guidelines, commitments, or ESG ratings. We also introduced disclosure levels and offered recommendations for how organizations could approach and adopt voluntary initiatives. These definitions and classifications are rapidly becoming standardized terms in the emissions management space.

We followed with our 2022 report, expanding our coverage to 24 voluntary initiatives available to the energy industry, including 8 new initiatives. The second edition leveraged questionnaires to collect detailed information from administering organizations. Using this data, we expanded the scope to include the entire supply chain, allowing participation for gathering, boosting, processing, transmission, and LNG operations. We also introduced a series of feature articles to help operators evaluate their voluntary options, with topics such as The Role of Measurement, Selecting the Right Initiative for You, Leaders in Differentiated Gas, and more.

This 2023 third edition updates existing and new programs, totalling 24 voluntary initiatives now available to the energy industry across the supply chain. New developments are highlighted as well as trends towards the use of shared methodologies and protocols among initiatives and regulatory bodies.

In 2022, there was a surge of adoption in most certification initiatives.

Most of these initiatives currently have a slow but steady rate of continued growth. OGMP 2.0 and MiQ are outliers, with 86% and 29% increase in number of listed participants, respectively.

Contrary to our expectations, we have found that less rigorous initiatives did not correlate to a higher uptake. Based on the data gathered, initiatives that rated themselves as moderate in the effort scale had the highest increase in uptake in 2023. This indicates that companies are willing to concentrate their effort on initiatives that have established their interoperability and value add, be it in terms of financial, operational and/or reputational value.

We also observed that most initiatives require or award higher ratings to companies employing direct emissions measurements. An Eye on Methane: International Methane Emissions Observatory 2022 Report noted direct measurement numbers were on average, 60% higher than industry estimation for United States energy production.

01. Participation is growing and seen across the world, especially for OGMP 2.0.

02. Most initiatives have acknowledged their complementary criteria with other programs, increasing interoperability and agility for participants.

03. Some regulatory bodies have started to structure their disclosure requirements around voluntary initiatives to streamline and maximize interoperability.

04. Measurement and reconciliation are now encouraged by multiple initiatives. ‘Measurement-informed inventories are gaining traction.’

05. Participating companies are facing heightened public scrutiny regarding their environmental claims, prompting administering organizations to improve on verifiability and transparency.

06. Newer initiatives are developing guidance for specific industries and segments.

While the cost of direct measurement is higher, measurement-informed inventories tend to better represent individual company inventories. Companies using direct measurement have more representative baselines giving higher credibility to their overall reduction results.

We identify six key knowledge gaps that may prevent broader industry uptake. Addressing these gaps and aligning protocols will improve transparency, credibility, and the value of voluntary initiatives.

In addition, we continue to address the knowledge gaps identified in the 2022 report. In particular, GTI Energy’s Veritas initiative has addressed the need for better data and more transparent reporting by creating methane measurement and reconciliation protocols. Amid continuous improvement, clarification, and recognition, we are optimistic that voluntary initiatives will become increasingly credible, trusted, and adopted within the oil and gas.

01. Harmonization between regulations and voluntary initiatives – Will initiatives adopt regulatory disclosure requirements, or the other way around? The alignment in their requirements will decrease the barriers in adoption of voluntary initiatives.

02. Chicken and egg conundrum: A major barrier in the adoption of certification and commitment initiatives has been the uncertainty around the benefits versus costs. However, a wide adoption of the initiative must happen to decrease this uncertainty.

03. How can administering organizations encourage transparency and accountability without dissuading companies from engaging in the programs?

04. What is the level of effort required and best approach for a credible measurement-informed inventory?

05. Encouraging companies to delve deeper into understanding their complete emissions profile through direct measurement remains to be a significant challenge.

06. There is no centralized and publicly accessible database that collects, aggregates, and analyzes information from the different initiatives. Is there a meta-initiative that can collect, aggregate, and disseminate reported data?

GHG’s are gases that trap heat in the atmosphere, and include carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), and fluorinated gases. Carbon dioxide and methane account for approximately 80% and 12% of total GHG’s respectively.

CO2 is produced by the combustion of fossil fuels or, in other words, the use of fossil fuels to create energy. Methane is produced during fossil fuel extraction (coal, gas, and oil), agricultural practices, land use, and by the decay of organic landfill waste.

Year over year methane emissions from energy combustion, leaks, and venting grew by 3% and 2% in 2021 and 2022 respectively1. Methane emissions are both harmful, and wasteful. The International Energy Agency (IEA) estimates that:

“More than 260 billion cubic metres (bcm) of natural gas is wasted through flaring and methane leaks globally today. It is unlikely that all of this can be avoided, but with the right policies and on-the-ground implementation on both flaring and methane emissions, an estimated 200 bcm of additional gas could be brought to markets.1 ”

In 2022 the average Henry Hub gas price was US$ 6.40/MMBTU. Using an average heat content of 1,037 BTU/cf, and 1 cf to 0.02833 m3, 1 bcm of natural gas is equal to 36,600,000 MMBTU. An additional 200 bcm could potentially translate to US$ 4.6 trillion in additional revenue.

01. Expanded analysis to include 3 new initiatives: Basinwide, Project Canary Low Methane Rating Protocol, and IFRS S1 and S2.

02. Full analysis coverage of initiatives across the entire supply chain, including gathering and boosting, processing, transmission, liquified natural gas (LNG), and distribution.

03. Comprehensive evaluations of new each initiative based on emissions reporting and public disclosure requirements, as well as its methodology transparency.

04. Year over year updates to existing initiatives noting changes or improvements against a consistent evaluation criterion.

05. Data driven results based on a survey of administering organizations, publicly available data, and published methodologies.

06. A series of feature articles on current trends and emerging paradigms, including:

a. Technology-driven developments and the adoption of measurements in carbon accounting.

Author: Dr. Thomas Fox, President & Chief Innovation Officer

b. What’s in it for Me? Natural Gas Voluntary Initiatives for Emissions Reductions.

Author: Paul Ashford P.Eng., Vice President of Consulting

c. Creating a demand-driven market for certified gas – the MiQ/Highwood index.

Author: Dr. Jeff Rutherford, Director of Research & Development

d. Balancing Access Against Climate Objectives.

Author: Heather Isidoro P.Eng., Senior Consultant, Voluntary Initiatives

While methane emissions from energy production are a fraction of carbon dioxide emissions, reduction of methane emissions can have a proportionately bigger impact that an equivalent reduction of carbon dioxide. In the atmosphere methane has a lifespan of 12 years, while carbon dioxide (CO2) can last for centuries. However, methane (CH4) has a much higher radioactive efficiency, or ability to absorb energy. When compared to carbon dioxide as a baseline, the Environmental Protection Agency (EPA) assigns a Global Warming Potential (GWP). The larger the GWP, the more significant the impact is on climate change. Methane has a GWP of 27-30 over 100 years, and 81-83 over 20 years, meaning the impact of methane reductions now can be 27-83 times more impactful than carbon dioxide reductions.

Many organizations continue to only meet the minimum regulatory requirements. Other organizations have scaled back from earlier announcements on energy transition and renewables to return to an emphasis on organic growth and sustainable cash flow. What will be the long-term cost of falling behind, or continuing to only meet the minimum regulatory requirements? Which strategy will ensure long-term stakeholder returns? For organizations that do choose to go beyond regulatory requirements, and prioritize strong ESG performance, what mechanisms are in place to help them stand out from their competitors, and give them an opportunity to showcase their performance?

Voluntary Initiatives are in the news and are represented on panels at every energy conference – but what are they, and why are companies doing them?

While the benefits to industry can be intangible or uncertain at this time, innovative and streamlined technologies are making it easier for companies to build emissions management into day-to-day operations and be recognized for it, thus turning participation in voluntary initiatives into a powerful business driver.

As methodologies improve and routine public disclosure becomes standardized, the benefits of Voluntary Initiatives will become more apparent and quantifiable. As stakeholders, including energy buyers and ESG conscious investors, continue to prioritize ESG alongside profit, organizations that go above and beyond minimum regulatory requirements will be rewarded. As standards and initiatives provide clearer paths and benefits, we expect Voluntary Initiative participation to increase as the industry works towards a shared vision of responsible energy.

Expanding on that structure in this 2023 report, we update the list of initiatives, perform new analyses, and deliver fresh insights. With so many Voluntary Initiatives to choose from, navigating the nuances and requirements to determine which initiative aligns with your corporate goals can be daunting. Our aim is to facilitate informed decision making on adoption of these initiatives by revealing their benefits and program particulars in an unbiased manner, making it easier for organizations to map out their emissions management journeys.

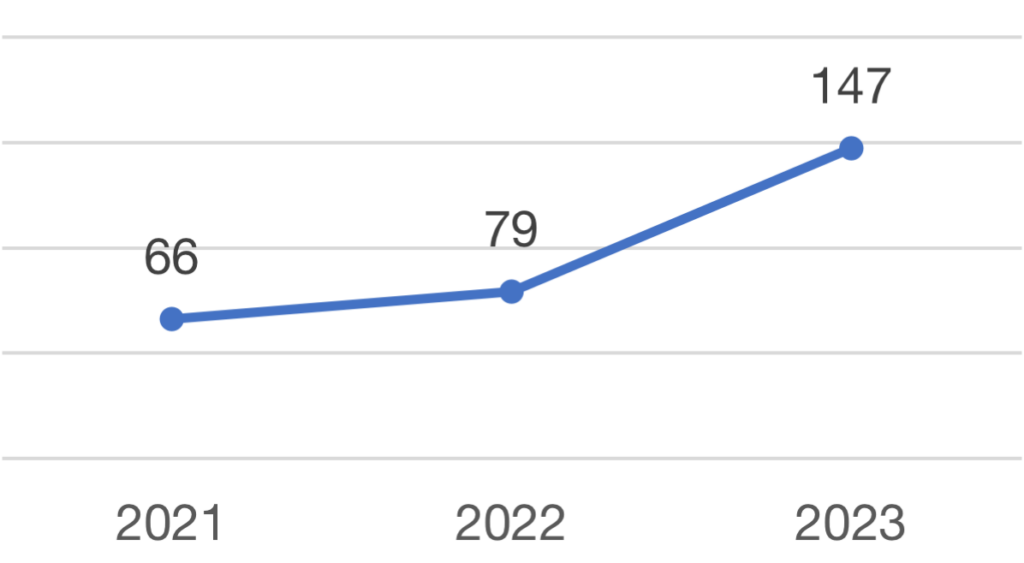

Our 2022 Voluntary Initiatives Report highlighted an increase in uptake for differentiated gas certification programs, such as MiQ and EO100. Similar trends have been observed for most other voluntary emissions reduction initiatives. While the rate of uptake is relatively high across the board, no single program compares to OGMP 2.0’s growth in the past two years: increasing from 66 companies in 2021 to 147 in 2023. Regulators, such as the Colorado Department of Public Health and Environment (CDPHE), are moving towards measurement-informed methane reporting and targets and are looking to harmonize their requirements with those of leading voluntary initiatives.

Please reach out with your questions, feedback, thoughts, or suggestions – we will listen as we continue to guide the industry through initiatives that reward industry for strong emissions performance.

The entity responsible for running a voluntary initiative and managing participation.

Emissions data that has been collected from multiple sources and summarized, usually for the purpose of public reporting or statistical analysis.

The ability to participate in multiple initiatives with lesser effort, often resulting from the interoperability of the initiatives

The verification of a participant’s data, practices, or performance by an entity other than the participant in question.

Designed to enable verification of a participant’s progress towards a goal or adherence to a voluntary initiative by an administering organization or independent third party.

A voluntary initiative that incorporates compliance measures.

An aggregate emission rate estimate achieved by multiplying activity factors (counts of components, equipment, or throughput) by emission factors (estimates of gas-loss rates per unit of activity). The vast majority of bottom-up inventories use emission factors derived from industry averages rather than measurements specific to the company. Bottom-up inventory emission rate estimates are consistently lower than site-level and regional emissions measurements in academic research. We avoid the term ‘top-down measurement’ in this report as it is imprecise and often leads to confusion.

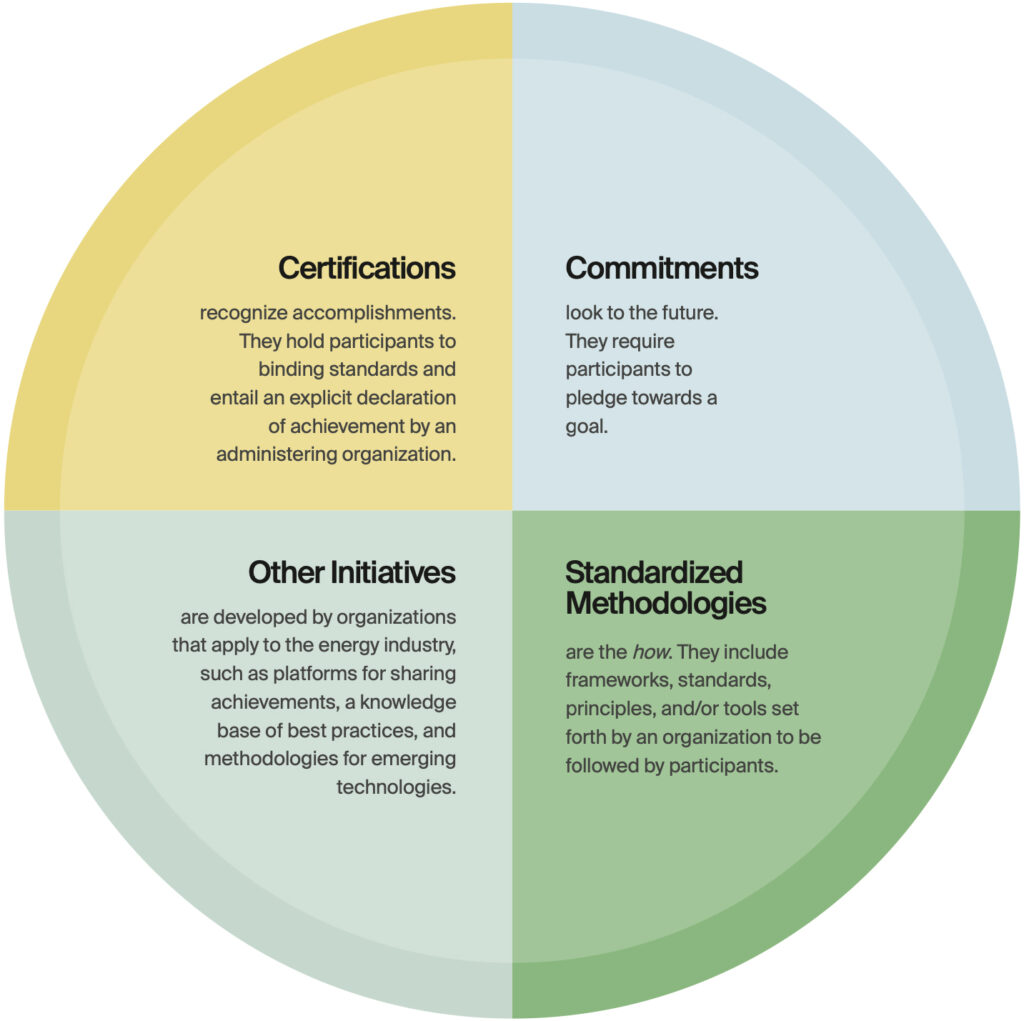

An initiative that holds participants to binding standards that may include emissions reduction performance targets, use of specific technologies, and/or adoption of methodologies. Certifications entail an explicit declaration of achievement from the administering organization to the participant.

A product (e.g., natural gas) that is distinguished from others on the basis of some attribute (e.g., emissions intensity), making it more attractive to a particular market.

The act of releasing information to a target audience.

A novel measure of disclosure for voluntary initiatives developed for this report.

A measure of the extent of participation in a voluntary initiative.

Greenhouse gas emissions, particularly carbon dioxide, methane, and nitrous oxides.

Initiatives that entail the full spectrum of reporting on Environmental, Social, and Governance topics.

An emissions quantification framework that is widely used by businesses, industry associations, NGOs, and other organizations. Some initiatives use the GHG Protocol for their emissions quantification requirements. GHG Protocol has published several standards, but is recognized for these two emission quantification guidelines:

Fostering an image of ecological responsibility that does not necessarily match, or only partially correlates, to the content of the communications transmitted.

A set of frameworks, standards, principles, and/or tools designed to assist participants in meeting their goals and reporting on their progress.

An initiative indicating that using other initiatives’ methodologies, data sets, and/or ratings and results to meet its own requirements are said to be interoperable with that other initiative. This often allows participants to be agile (see Agility).

Acquiring emissions data directly from the environment at a specific place and time.

Pertaining to emissions, achieving a state where either no greenhouse gases are emitted, or remaining emissions are offset through other actions or technologies that can capture or remove carbon from the atmosphere.

Greenhouse gas emissions can be estimated using emissions factors, measurements, or engineering equations at various spatial and temporal scales. Reconciliation explores whether and why different estimation approaches vary. In some cases, reconciliation can be defined as a methodology for combining multiple different estimates into a single stronger estimate.

Mandatory submission of emissions data to a government body.

Any company, organization, institution, regulatory body, or other entity that participates in a voluntary initiative.

Natural gas that meets standards set out in a voluntary initiative. Note that the precise definition of responsible gas is not consistent across initiatives.

Scope 1 or direct emissions are those emissions arising from sources owned or controlled by an organization within a defined boundary.

Scope 2 emissions are indirect emissions from the generation of purchased energy, from a utility provider.

Scope 3 emissions are all indirect emissions – not included in scope 2 – that occur in the value chain of the reporting company, including both upstream and downstream emissions.

Also referred to as the energy value chain, the sequential segments of product flow from initial production through end use. For gas production, the segments commonly include production, gathering and boosting, processing, transmission, storage, distribution, and possibly LNG liquefaction, shipping, and regassification.

The degree to which an initiative or participant discloses their internal operations and standards and allows for accessibility of information regarding an initiative.

See “Supply chain”

A coordinated effort managed by an administering organization that enables participants to take standardized voluntary steps towards targeting, achieving, and/or taking credit for emissions reductions.

President and Chief Innovation Officer

Highwood Emissions Management

Over the past decade, the field of methane emissions monitoring has undergone rapid and diverse technological advancements. What began with a few handheld solutions has now expanded to encompass an array of novel methods, including drones, continuous monitors, satellites, aircraft, and even vehicle-based systems. Highwood Emissions Management, a recognized authority in this domain, has been tracking and assessing these evolving solutions through rigorous field testing and simulation modeling. Our proprietary database presently catalogues more than 200 commercially available methane detection and quantification technologies.

Each time you blink, these technologies become increasingly diverse. They exhibit significant variations in spatial and temporal resolution, methane sensitivity, environmental constraints, reliability of performance testing outcomes, and data characteristics. These discrepancies highlight the complexity of emissions monitoring and pose both challenges and opportunities for those engaged in carbon accounting.

Historically, methane monitoring technologies have predominantly served Leak Detection and Repair (LDAR) programs, aimed at promptly identifying and addressing leaks. However, a trend has emerged in recent years, marked by a transition from leak detection to a more comprehensive approach involving emission rate quantification.

Emission rates are calculated by extrapolating from samples across spatial and temporal dimensions, thereby estimating a company’s total emissions over a given period. While the science behind these estimations is relatively novel and characterized by large uncertainties, regulatory bodies such as the Colorado Department of Public Health and Environment (CDPHE) and the Environmental Protection Agency (EPA), along with initiatives like OGMP 2.0, MiQ, and Veritas, are increasingly mandating the collection and reporting of emission rate estimates derived from top-down measurements.

As the adoption of measurement-based emission rate estimates gains traction, the challenge of comparing and combining disparate datasets will grow. Despite the rise of direct measurement, it’s widely acknowledged that such data has inherent limitations, leading to the need for reconciliation.

Reconciliation involves the integration or comparison of measurement data with bottom-up inventories, the specifics of which vary based on regulatory standards or voluntary initiatives. The goal is to harness the strengths of both measurement data and traditional inventories, leading to more accurate, comprehensive measurement-informed inventories.

The increasing prevalence of measurement-informed inventories underscores the urgency for operators to develop expertise in handling measurement data and reconciling it with bottom-up inventories. A significant outcome of this reconciliation process is the potential of higher estimates of annualized methane emissions. This discrepancy arises due to the tendency of bottom-up inventories to consistently underreport emissions, particularly within the production and midstream sectors.

The convergence of technological innovations and carbon accounting practices has generated a dynamic and transformative landscape. From the proliferation of methane monitoring solutions to the significant shift from leak detection to quantification and the pivotal role of reconciliation, these developments underscore the evolving nature of carbon accounting. As stakeholders navigate new opportunities and obligations, embracing innovation while mastering the intricacies of measurement data and reconciliation will empower energy companies to thrive amid a transforming energy economy.

P. Eng., Vice President of Consulting

Highwood Emissions Management

With growing concerns about climate change and GHG emissions, companies in the energy industry are increasingly exploring voluntary initiatives for emissions reductions. While regulatory requirements set minimum standards for each jurisdiction, companies that go beyond these requirements can reap numerous benefits, and voluntary initiatives for emissions reductions have gained momentum. This special feature explores why a company that to date has followed a minimum regulatory compliance approach should be interested in voluntary initiatives, whether such initiatives are becoming table stakes, and what the future holds for the industry.

In many jurisdictions, gas producers are required to obtain and maintain licenses to operate. Regulators assess a company’s compliance with environmental regulations, social impacts, and sustainability practices when granting and renewing these licenses. By engaging in voluntary initiatives for emissions reductions, gas producers demonstrate their commitment to exceeding regulatory requirements, strengthening their position for obtaining or maintaining operational licenses. By showcasing proactive efforts to mitigate environmental impact, companies align with regulatory expectations for responsible operations.

The investment landscape is increasingly considering ESG factors. Many investors, including institutional funds and asset managers, prioritize investing in companies that demonstrate strong ESG practices and are growing increasingly savvy in their expectations for tangible demonstration of minimized environmental impact. Securities regulators in the United States and Canada are proposing mandatory emissions disclosure for publicly traded companies. Participating in voluntary initiatives for emissions reductions can showcase a gas producer’s commitment to sustainability and responsible business practices, making it more attractive to ESG-focused investors. This, in turn, can lead to increased investment opportunities, access to green capital, and potentially lower cost of capital. Companies that proactively address environmental impact are seen as more resilient and better equipped to navigate the transition to a low-carbon economy, making them attractive to long-term investors.

Insurance companies are increasingly factoring in environmental risks when underwriting policies. By actively participating in voluntary initiatives for emissions reductions, gas producers demonstrate their commitment to environmental stewardship. This can lead to more favorable insurance terms, including lower premiums, as insurers perceive lower risk associated with companies that prioritize sustainability. Additionally, demonstrating proactive measures to manage emissions can reduce the risk of future environmental liabilities, further enhancing insurability.

In today’s market, sustainability and responsible business practices have become key differentiators. Consumers are increasingly considering the environmental impact of the products and services they choose. By participating in voluntary initiatives for emissions reductions, companies will position themselves as leaders in the industry, gaining a competitive edge over peers who only meet the minimum requirements.

As sustainability becomes a significant factor in consumer purchasing decisions, companies that exceed minimum regulatory requirements can differentiate themselves in the market. By highlighting their commitment and progress on emissions reductions, gas producers can attract environmentally conscious customers. This creates brand loyalty and positive brand perception, furthering their competitive advantage over those who have not made similar commitments.

The potential to receive premium pricing for low-methane gas has been touted as an additional benefit for several certification initiatives. While we have seen instances of premium pricing on bilateral marketing contracts, there has yet to be widespread evidence of premium pricing for certified gas. There is possibility for greater instances of premium pricing as consumers and purchasers begin to value and demand energy that is produced to the highest environmental standards.

Voluntary initiatives for emissions reductions are becoming increasingly important in the context of the evolving energy landscape. Governments, businesses, and consumers are demanding greater action to combat climate change and reduce GHG emissions. As a result, regulatory requirements are expected to become more stringent in the future.

By embracing voluntary initiatives today, gas producers can prepare for a future where emissions reductions and sustainability are the norm. Investing in cleaner technologies, optimizing operational processes, and adopting innovative approaches can help companies stay ahead of regulatory changes, meet evolving stakeholder demands, and future-proof their business.

Moreover, the transition to a low-carbon economy presents opportunities for innovation and collaboration. Gas producers that actively engage in voluntary initiatives can contribute to industry-wide knowledge sharing and technology advancements. By working together, the industry can develop and deploy more sustainable practices, driving the transition to a cleaner energy future.

An intangible benefit for companies participating in voluntary initiatives can be the positive impact on their reputation. Investors are increasingly factoring ESG criteria into their decision-making process. By actively participating in voluntary initiatives, gas producers can attract ESG-focused investors and access funding opportunities that may not be available to companies that only meet minimum regulatory requirements.

By voluntarily exceeding regulatory requirements, companies can showcase their commitment to sustainability and environmental stewardship and contribute in a tangible way to global efforts to combat climate change. This can further enhance a gas producer’s reputation by showcasing their willingness to proactively addressing emissions management and reductions, companies will position themselves as leaders in the industry, enhancing reputation and credibility. It aligns and builds trust with the increasing expectations of consumers, investors, and stakeholders who prioritize sustainability and responsible business practices.

In conclusion, voluntary initiatives for emissions reductions offer numerous benefits to gas producers. From enhancing reputation and gaining a competitive advantage to accessing new markets and investment opportunities, there are clear incentives for companies to go beyond the minimum regulatory requirements. By actively participating in voluntary initiatives today, gas producers can position themselves as leaders in sustainability, contributing to a greener future and ensuring long-term success in a rapidly evolving energy landscape.

Director of Research & Development,

Highwood Emissions Management

In countries like the United States and Canada, operators are required to disclose methane emissions via government-led reporting programs (i.e. U.S. Greenhouse Gas Reporting Program). Over the past decade, studies based on novel methane measurement technologies have revealed potential inaccuracies in government-led programs, often a significant downward bias. This has eroded trust among gas buyers and the public in government-led reporting programs and the natural gas industry in general.

Third party certifiers such as MiQ, Equitable Origin, and Project Canary’s TrustWell provide alternative avenues for natural gas operators to report methane emissions and other environmental attributes of their operations. In theory, gas volumes certified by third-party programs will be more attractive to ESG-conscious investors and buyers. As ESG pressures mount, and pending significant improvements in government-led reporting, natural gas operators are incentivized to improve operational efficiency. Those with the highest environmental performance, lowest methane emissions, and emission reductions will be selected above others.

What level of methane emissions from a natural gas operator should be considered strong environmental performance? This relates to a general challenge in environmental certification programs, which is setting a benchmark and determining what is good, better, or worse than the average. Credible, reproducible benchmarks are also critical in any financial instrument, much like the S&P 500, for backing performance claims and any resulting financial transactions.

To date, assessing overall industry average methane emissions has been complicated by the breadth of the industry, difficulties in measuring at a large enough scale, and the varying nature of methane emissions sources. In the United States alone, assessing >1 million wells, millions of miles of pipeline, and hundreds of processing and transportation facilities is an enormous undertaking. The U.S. Environmental Protection Agency’s Greenhouse Gas Inventory is the most often used as an industry baseline, however, as mentioned above, this underestimates emissions in many cases. A low baseline derived from inaccurate emission factors disincentivizes participation in voluntary initiatives by underestimating the benefits to high-performing operators and those that chose to quantify and disclose their emissions more fully.

Highwood’s understanding of emissions in the natural gas industry has improved substantially beyond the methodology underlying the Greenhouse Gas Inventory. Private and public-led initiatives have launched aerial methane measurement technologies capable of gathering data at a rapid rate. In a recent preprint, Sherwin et al. summarized several years of data from aerial methane measurement technologies surveys (specifically Kairos Aerospace and Carbon Mapper) over one million sites. The aggregate measurements are approximately three orders of magnitude higher than previous synthesis work, making this the most comprehensive synthesis study to date.

In a subsequent white paper titled “The MiQ-Highwood Index™: A national-scale measurement-informed methane intensity for the United States”, Highwood and MiQ reviewed the methane emissions data synthesized in Sherwin et al. This analysis led to the creation of the first open-access measurement-informed methane intensity index for the U.S. natural gas sector. Methane intensity is defined here as methane emitted normalized to methane produced.

Extrapolating results from Sherwin et al. to the U.S. lower 48 onshore energy industry, Highwood and MiQ calculate a methane intensity of 1.0% for production operations and 2.2% for the full supply chain (values allocated to the natural gas product). However, the Sherwin et al. preprint is limited to the high-productivity Pennsylvania zone of the Appalachia basin. More data collection is required to accurately assess individual basin intensity variations. As new data becomes available, the index will be updated.

The MiQ-Highwood Index™ provides gas buyers the information to understand the environmental performance of their supply chain relative to the national average. improving the buyer’s confidence in accessing the certified gas market.

P.Eng., MBA, Senior Consultant,

Voluntary Initiatives, Highwood Emissions Management

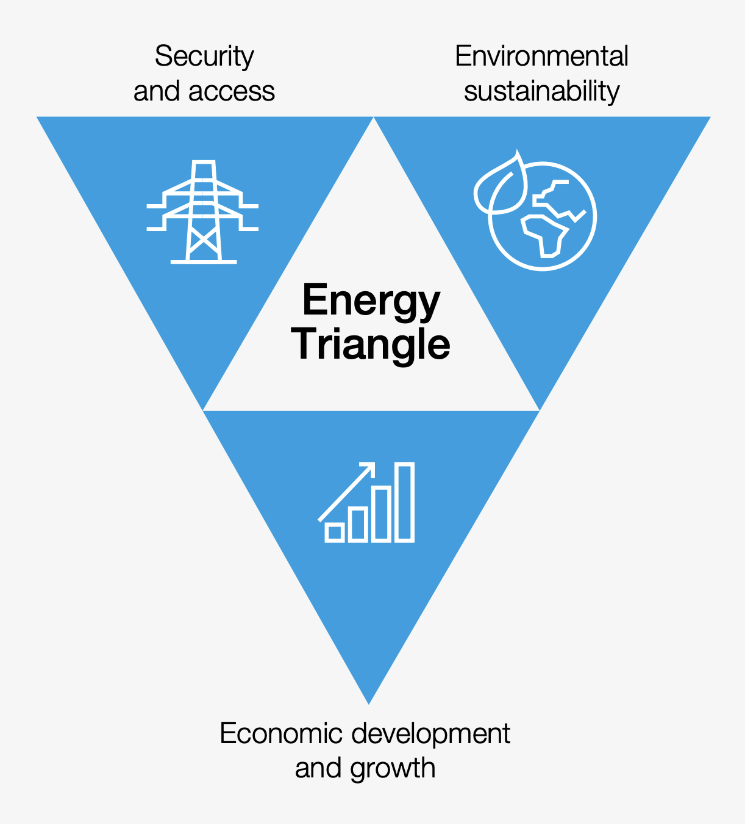

As the world strives to achieve the climate goals set out in the 2015 Paris Agreement, parts of the world still do not have access to a single, basic, reliable energy source. As this, and other factors, continue to contribute to rising global energy demand, the energy industry has an important part to play. As the industry faces pressure to reduce GHG emissions, those who proactively exceed the regulatory requirements are starting to be rewarded. By participating in Voluntary Initiatives, energy companies are distinguishing themselves and leaders in clean-er energy, balancing both rising demand, and climate objectives.

Approximately 1 billion people still lack reliable access, or any access, to electricity. While environmental concerns are the driver behind energy transition, transition cannot be achieved at the expense of economic sustainability and development, or access to reliable energy. As the world population surpassed 8 billion in 2023, energy demand continues to increase, rather than decrease.

While the term energy transition is broadly thrown around, it is a common assumption that transition means moving completely away from fossil fuels to renewable sources of energy. However, this rising demand cannot be met without fossil fuels in the foreseeable future.

The concept of energy transition was first used by United States President Jimmy Carter in an address on the Nation of Energy regarding the 1970’s energy crisis:

The World Economic Forum states, “energy transition is about more than decarbonization”⁴. While historical transitions were driven by availability of resources and cost, today’s transition is driven by environmental factors and the global effort to minimize climate change. However, the current transition is not simply about replacing fossil fuels.

Energy transition does not replace one source of energy with another. Throughout history, as new energy sources were discovered and commercialized, the transformation was gradual. Coal did not immediately replace wood but was incorporated alongside it until it became an economic and widespread source of energy. Similarly, energy did not replace coal, but was supplementary to coal, competing in cost and efficiency.

For this current transition to be successful the energy triangle needs to be balanced. Transition, or transformation, cannot be achieved at the expense of access or economic stability.

There is not one path to transition, but many paths that can be taken to develop cleaner sources of energy. While many immediately assume clean equates to renewables, increased efficiency and emissions mitigation of current energy sources is equally important. Generally considered a key contributor to climate change, the energy industry can also play a strategic part in transitioning the world to clean-er energy by participating in Voluntary Initiatives and exceeding regulatory minimums.

In an era of transition, where renewables also reached record high share of generation, 2021 and 2022 saw coal emissions grow year-over-year to record highs. As many countries undertake coal to gas initiatives, countries like China, India, Japan, Indonesia, and Vietnam continue annually to increase coal capacity. While developed countries push for clean energy, developing countries simply want access to energy. Fluctuating natural gas prices have even prompted some north American power producers to shift from natural gas back to coal to protect the bottom line.

In 2022 energy-related GHG emissions peaked at 41.3 Gt7 of CO2 equivalent, an increase of 6% from 2020-2021, and an additional 1% from 2021-2022⁵. The anthropogenic emissions (emitted by human activity) from carbon dioxide and methane account for approximately 89% and 10% of that total respectively⁵. Energy related carbon dioxide emissions are caused by fossil fuel usage, and the largest driver of growth was electricity demand. Energy related methane emissions are caused by venting, flaring, and leakage in the systems that produce and transport fossil fuels.

While renewables continue to develop alongside fossil fuel, the energy industry has an opportunity to make a significant positive climate impact.

Diversifying and developing renewables are both capital intensive and require expertise and capabilities that are not always aligned with traditional energy expertise or operations. According to the International Energy Agency (IEA), less than 1% of total capital expenditures of the energy industry is invested in diversifying outside of core traditional operations.⁵

Energy demand is beyond the industry’s control and is driven by consumerism and a growing global population. Meeting that demand today requires fossil fuels, however, companies can undertake initiatives to lower the intensity of their operations. By reducing emissions from existing and new operations, energy companies can differentiate themselves to stakeholders who prioritize ESG performance alongside financial, and in some cases even profit from it.

“As of today, 15% of global energy related GHG emissions come from the process of getting energy out of the ground and to consumers. Reducing methane leaks to the atmosphere is the single most important and cost-effective way for the industry to bring down these emissions.”⁵

The IEA estimates that emissions could be reduced by almost 40% through methane reductions, reduced flaring and venting, and efficiency improvements by 2030⁶. Reducing emissions in this space requires more accurate quantification to accurately track reductions. By participating in Voluntary Initiatives, companies have access to the tools, support, frameworks, and markets to set and realize the benefits of targets that go beyond the minimum requirements. Energy producers can position themselves as leaders in energy transformation, setting standards to meet both rising future demands, alongside climate objectives.

The following are insights derived from the information gathered, and on news and developments of each initiative.

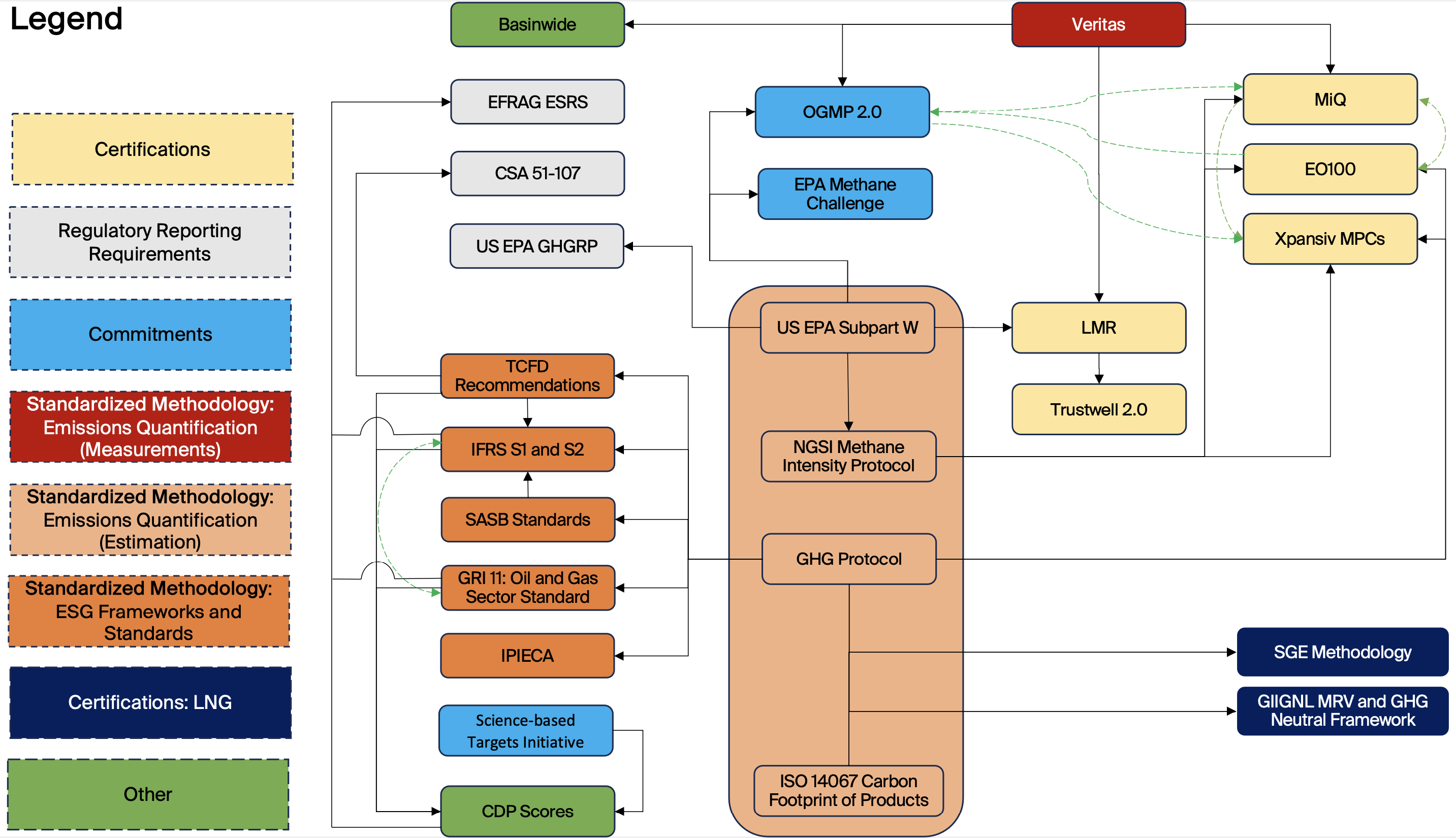

Establishing alignments and partnerships between initiatives provide participants the agility to achieve multiple programs using one set of data. For example, producers reporting to the US Environmental Protection Agency’s GHG Reporting Program will already have their emissions quantification using Subpart W guidelines. These producers are in a good position to access OGMP 2.0, the EPA Methane Challenge, Project Canary’s Low Methane Rating.

The availability of the Veritas protocols standardizes the measurement and reconciliation process, allowing certifications such as MiQ and the Low Methane Rating Protocol to point to Veritas for measurement and reconciliation methodologies.

Participants know their emissions profile better and can make informed decisions to select the best available measurement technology that fits within their purposes and budget.

Most initiatives share company-specific or anonymized emissions data with the public, including methane targets and aggregated source-level emissions. Initiatives that do not have specific rules on public disclosure have noted that the participating companies can still release the information at the companies’ discretion.

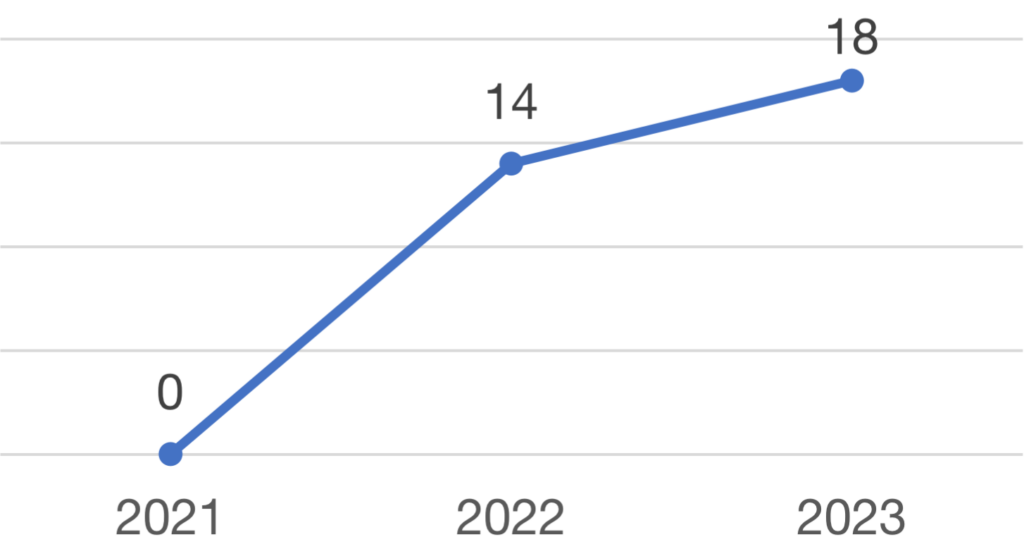

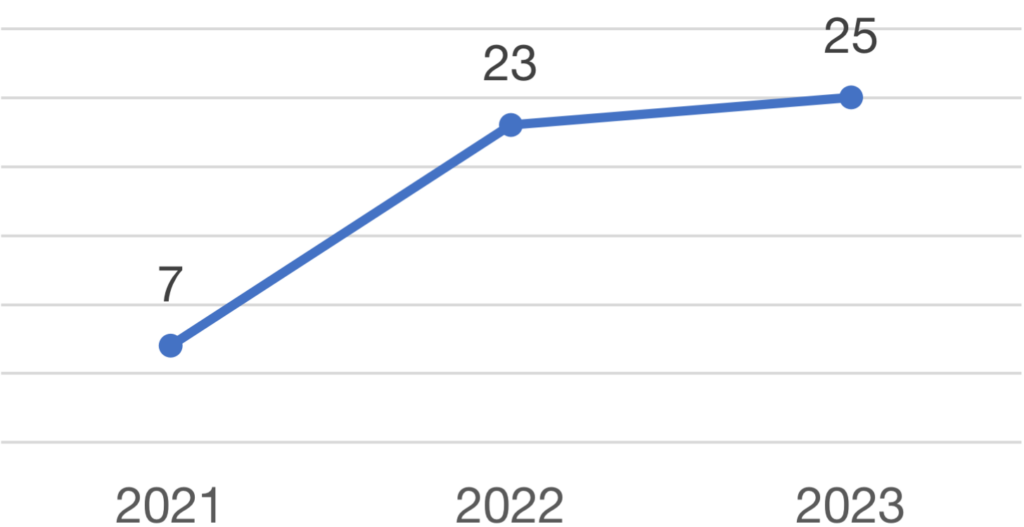

In 2022, we saw certifications taking the lead in increased uptake. For 2023, we are seeing a shift of uptake leaders: OGMP 2.0 almost doubled their participants from last year’s count. MiQ and EO100 still have higher uptake than most initiatives.

However, the rate of uptake did not correlate with the required effort. Based on the data gathered, initiatives that rated themselves as moderate in the Effort scale had the highest increase in uptake in 2023. This indicates that companies are willing to concentrate their effort on initiatives that have established their interoperability and value add, be it in terms of financial, operational and/or reputational value. Once potential participants see these from an initiative, the required effort will likely cease to be a barrier.

| Initiative | Category | 2022 participants | 2023 participants | Effort |

|---|---|---|---|---|

| Oil and Gas Methane Partnership (OGMP) 2.0 | Commitment | 79 | 147 +86% | Moderate |

| The MiQ Standard | Certification | 14 | 18+29% | Moderate |

| EO100™ Standard for Responsible Energy Development | Certification | 23 | 25+9% | Moderate |

| The Environmental Partnership | Commitment | 97 | 102+5% | Low |

| EPA Methane Challenge | Commitment | 69 | 71+3% | Low |

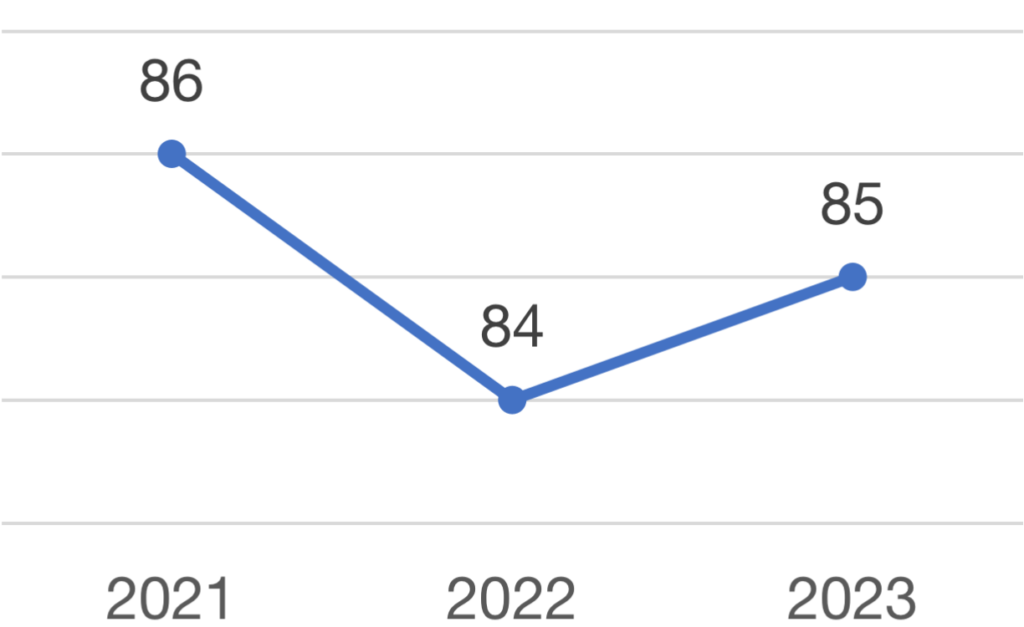

| MRV and GHG Neutral LNG Framework | Certification | 84 | 85+1% | Moderate |

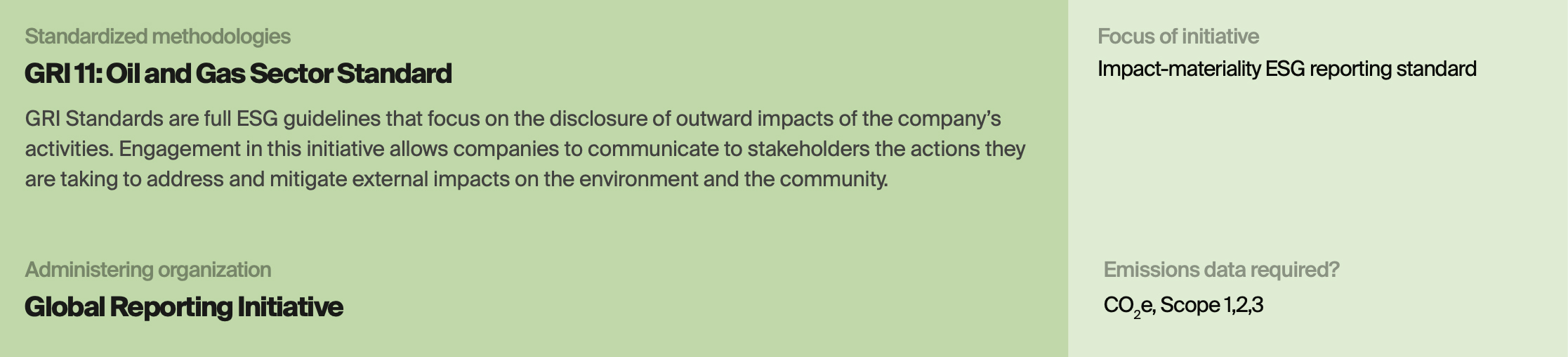

European Sustainability Reporting Standards are now aligned with International Sustainability Standards Board (ISSB) and Global Reporting Initiatives (GRI) disclosure standards, while Canadian Securities Administrator (CSA) has aligned CSA 51-107 with the Task Force on Climate-Related Financial Disclosures (TCFD) Recommendations.

This chart depicts the interrelations between different initiatives and existing regulatory mandates. Solid lines indicate the integration of standardized methodologies across voluntary initiatives and regulations, while dashed lines represent the interconnectedness of initiatives, showcasing their complementary and overlapping criteria.

This pressure drives administering organizations to develop their initiatives around transparency and verifiability, and for companies to be conscious about greenwashing and be aware of the reputation of the initiatives they participate in.

All initiatives in the Certification category require either a third-party audit or an internal audit of the participants’ data. Most administering organizations also make their methodologies accessible to the public for full transparency.

While we are seeing an increased interest in certified gas, the benefits to buyers of certified gas remains a gap that administering organizations need to establish and quantify. Additionally, companies looking to reduce their Scope 3 emissions tend to go for nature-based offset products instead of the low-methane products. These offset products tend to be abundant in supply across multiple project types and are easier to access through multiple registries, such as the Verra Registry and the Impact Registry.

Only six LNG cargoes are known to have received emissions statements since the inception of LNG-specific certification programs.

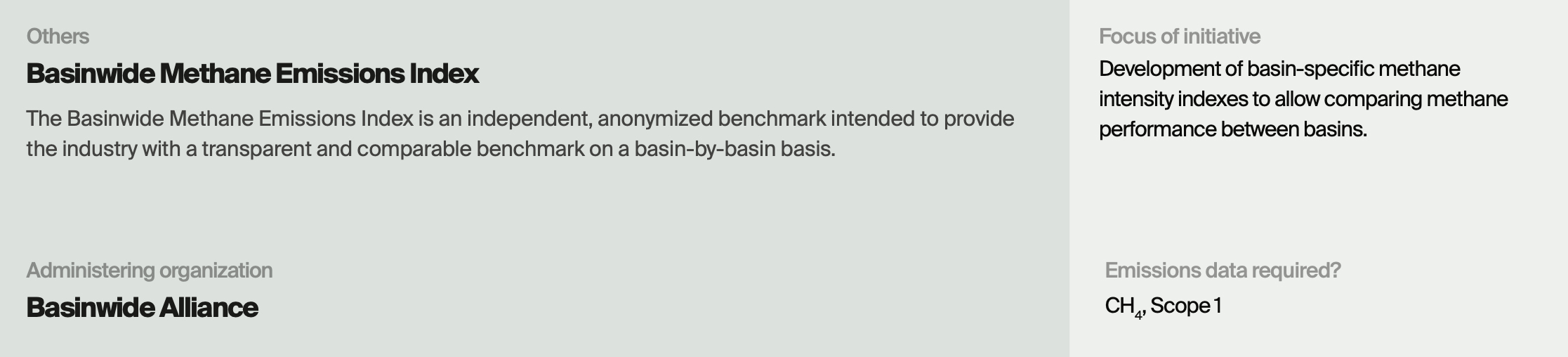

Xpansiv launched the Digital Fuels Program 2023 Methane Emissions Benchmark, MiQ published the MiQ-Highwood Index, and the Basinwide Alliance has publicized plans to establish the Basinwide Methane Emissions Index.

Understanding these intricate relationships empowers participants to become agile in efficiently navigating through multiple initiatives and regulatory requirements. For example, a company working to meet requirements using NGSI Methane Intensity Protocol for EO100 certification can simultaneously fulfill prerequisites for other initiatives that use NGSI, such as Xpansiv MPCs.

Likewise, participants in OGMP 2.0 can obtain MiQ certification by employing identical methodologies to quantify emissions. Companies with certified methane emissions under MiQ standards can further attain full ESG verification through EO100.

We are seeing some gaps from the 2022 Report being addressed by one or more organizations, while others have not yet been addressed.

| Gaps in 2022 | Progress in the past year |

|---|---|

| How can consolidation and harmonization of initiatives improve? | Multiple organizations, including regulatory agencies, have expressed their existing interoperability with other organizations. (See Key Findings section) |

| How can emissions measurement technologies be used to collect meaningful data? | Carbon Mapper, a non-profit organization, has made publicly available their top-down methane and carbon dioxide emissions measurement data. |

| How should reconciliation of measurements and bottom-up inventories be performed? | GTI Energy’s Veritas initiative has stepped up to provide guidance on conducting measurements and performing reconciliation. |

| Is there a meta-initiative that can collect, aggregate, and disseminate reported data?

How can more robust and transparent differentiated gas markets be established? |

No significant progress was noted over the previous year |

Will initiatives adopt regulatory disclosure requirements, or the other way around? The alignment in their requirements will decrease the barriers in adoption of voluntary initiatives.

A major barrier in the adoption of certification and commitment initiatives has been the uncertainty around the benefits versus costs. However, a wide adoption of the initiative must happen to decrease this uncertainty.

Potentially discouraging companies from joining an initiative. How can we maintain our efforts to encourage transparency and accountability without dissuading companies from engaging in the programs?

Encouraging companies to delve deeper into understanding their complete emissions profile through direct measurement remains to be a significant challenge.

Gaining insights from the information amassed by these initiatives holds significant potential for regulators, educators, and other stakeholders involved in shaping a global strategy for mitigating methane and other GHG emissions.

01. Administering organizations must capitalize on their successes by quantifying the benefits of participation, not only to increase buy-in, but also to identify opportunities for alignment with similar initiatives.

02. All stakeholders should continue to collaborate, establish alignments, and work towards consolidation of complementary programs to provide companies with the agility to participate in multiple initiatives using the same set of data.

03. Administering organizations should continue promoting transparency and move towards requiring independent verification to increase the credibility of their programs, shield participants from possible allegations of greenwashing, and enhance stakeholder confidence

04. The energy industry should lead by example and promote better emissions quantification, reporting, and mitigation to encourage other industries to follow suit.

The 2023 edition of the Highwood Voluntary Initiatives Report includes 24 voluntary initiatives grouped into these four categories:

Additional information on each initiative can be found in the appendices.

Additional information on each initiative can be found in the appendices.

Additional information on each initiative can be found in the appendices.

It is important to note that Highwood does not consider any one initiative to be “better” or “worse” than any other based on the applicability of the categories. Each type of initiative has a unique approach to engaging with industry and recognizing the efforts made by the participants. Highly rigorous initiatives set high standards, but they also present financial and logistical barriers for companies who are not ready for that level of commitment. Initiatives with less stringent requirements enable broader participant and provide an important gateway towards greater action.

* Information is limited to publicly available data and to data provided by the administering organizations to Highwood.

Note: These links have been provided to help guide you through methane requirements, resources, and initiatives. All links are current to our knowledge as at the time of publishing this report. We cannot guarantee that links are accurate or up to date.

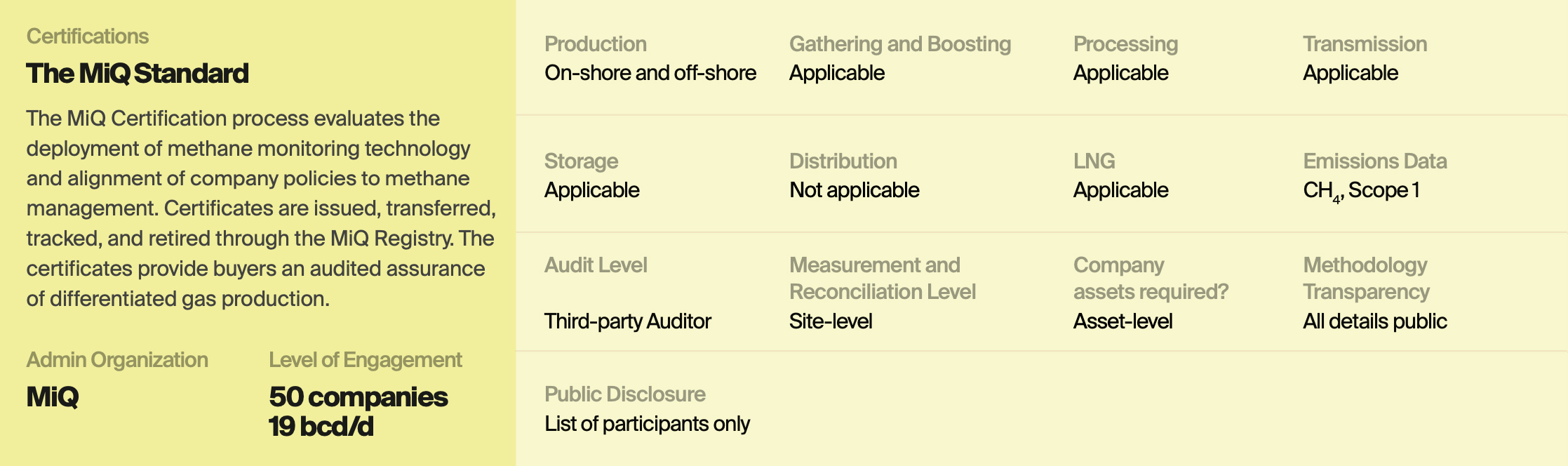

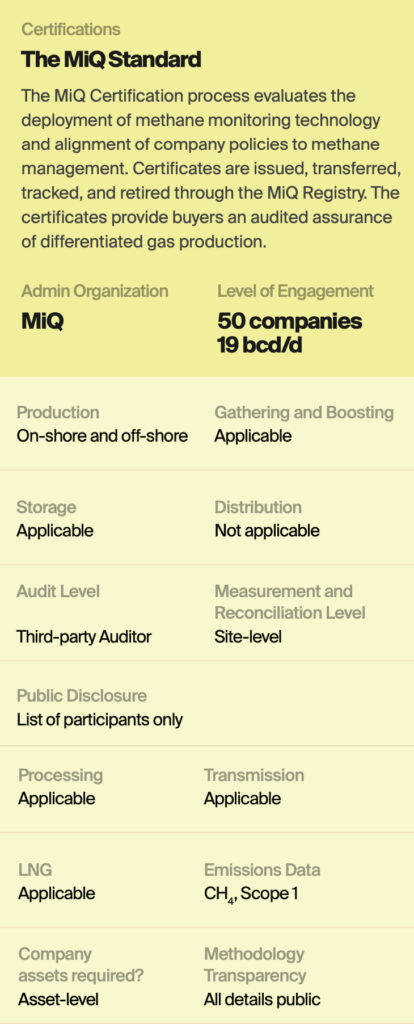

The MiQ Standard is an independently audited certification initiative that promotes holistic evaluation by requiring operators to disclose their methane emissions intensity, deploy advanced methane monitoring technology, include all detected events into their emissions inventory, and implement emission control best practices.

Companies certified in MiQ enjoy the benefits of having differentiated gas. Operators use the MiQ Registry, MiQ’s certificates-tracking hub, to attract buyers who are looking for accountable and verifiable energy for their own emissions management initiatives. The MiQ Registry provides the platform for tracking certificates from inception to retirement/end-of-use – as the physical gas moves, so do the certificates.

01. Updated Onshore Production and Offshore Production standard for Methane Emissions Performance

02. Released Gathering & Boosting, Processing, Transmission & Storage, and LNG standard for Methane Emissions Performance

03. Released Greenhouse Gas Intensity Standard for all segments

04. Released MiQ-Highwood Index

Scope 1 for Methane Intensity, Scope 1 and 2 for GHG Intensity, and certificates can be transacted for Scope 3 attestations

Fully implemented

2020

Privately funded non-profit

Global

Moderate

All oil and gas industry segments, including LNG liquefaction, shipping and regasification

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

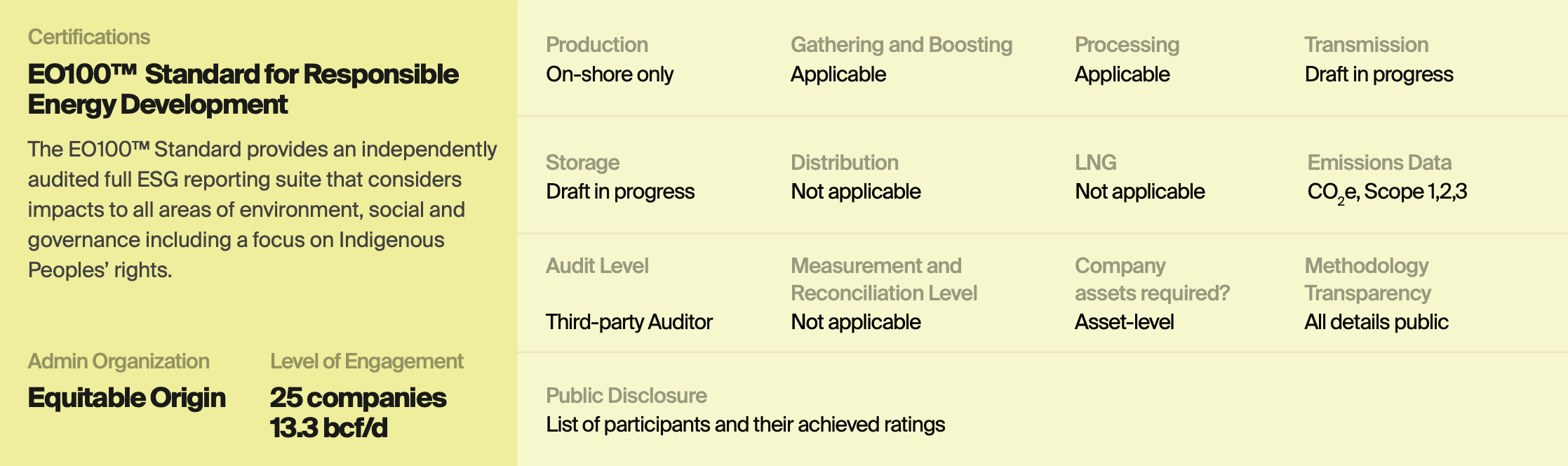

EO100™ is technology neutral with publicly available methodologies and resources, and it is audited by third-party organizations. Certifications are issued on an asset-level, and there is no allowance for partial certifications within a given boundary or basin.

In 2021, EO and MiQ started working together to issue joint certifications. This partnership is expected to yield additional uptake of participants in the coming years.

EO100™ has shifted from a pass/fail rating system to letter grade scoring in 2023. By switching to letter-based grading, EO100™ aims to incentivize producers to improve over time. The new grading system requires a minimum score of 70% under each of the standard’s five principles to get certified.

www.energystandards.org

Scope 1, 2 and 3

Equitable Origin

Fully implemented

2009

Privately funded non-profit

Global

Low cost, moderate effort

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

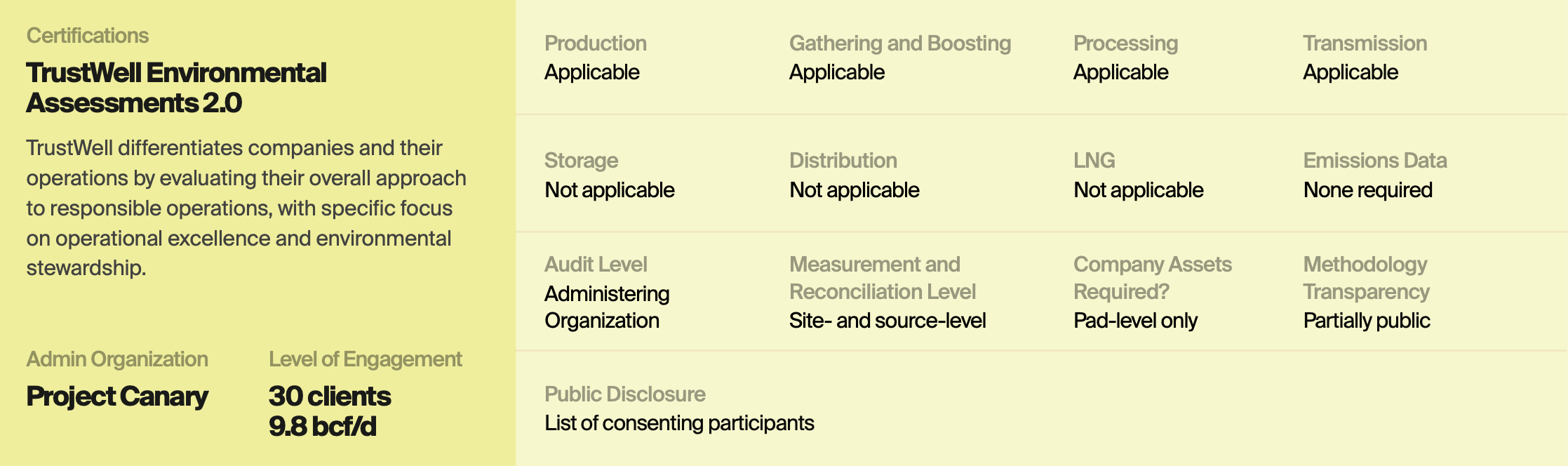

Project Canary’s TrustWell Environmental Assessment differentiates companies and their operations by evaluating their overall approach to responsible operations, specifically regarding operational excellence and environmental stewardship. TrustWell provides a cost-effective environmental assessment based on engineering risk and environmental mitigation.

A performance score is provided for each individual asset undergoing the assessment. Embedded in these scores are a producer’s operational insights, benchmarking data, and tradable, registry-ready environmental attributes.

Operators can then place these performance ratings on a digital registry, such as Xpansiv’s CBL. Additionally, operators can use their assessment to prioritize operational changes within their assets to improve efficiencies and overall environmental performance.

Project Canary maintains an ongoing relationship with all participants of the TrustWell program. This level of engagement provides operators with a path toward continuous improvement across all environmental attributes.

N/A

Project Canary

Fully implemented

2022

Privately funded for-profit

Global

Low cost, moderate effort

Environmental and social considerations

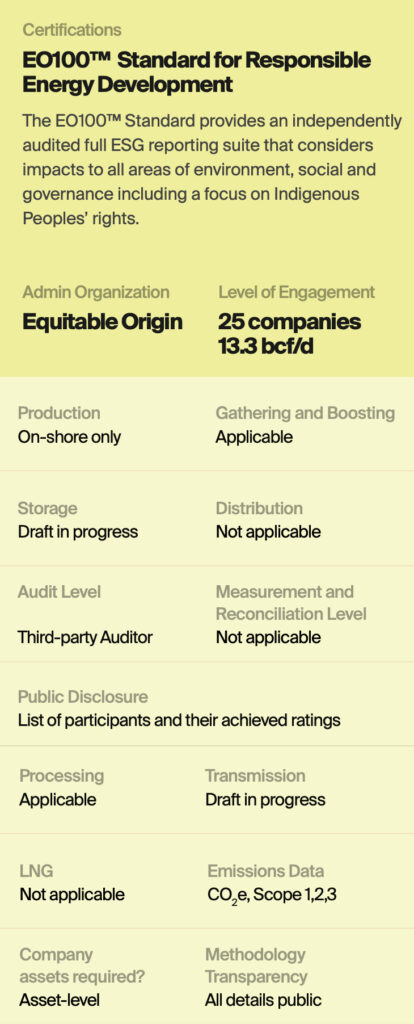

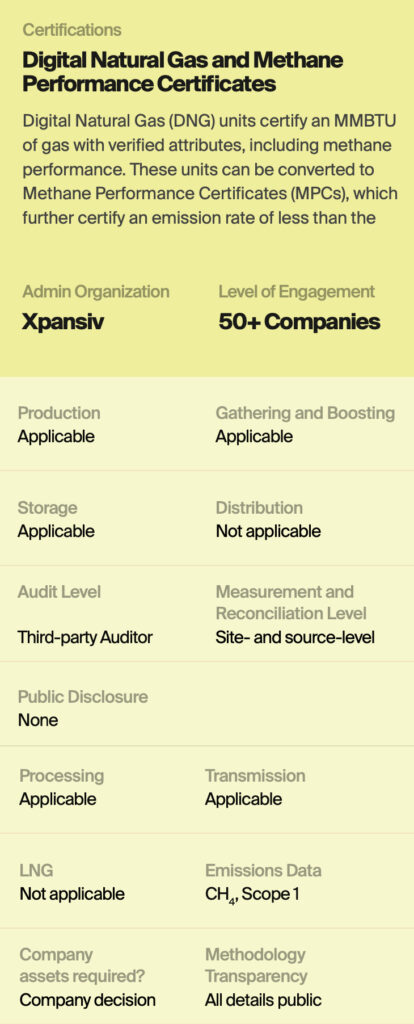

DNGs and MPCs are two of many certification programs in Xpansiv’s Digital Fuels Program. The environmental performance metrics encrypted into DNG are derived directly from empirical production and environmental monitoring data. Producers that register DNGs and MPCs have an immutable record of the environmental data of specific units of gas, including their methane performance.

The Digital Fuels Program, which the DNG and MPC products are part of, aspires to drive the transition to low carbon energy with a new class of standardized environmental attributes that differentiate fuels based on ESG performance.

Digital Natural Gas units having methane emissions intensity lower than 0.1% qualify for conversion to MPCs.

The Digital Fuels Program updates their baseline rate of methane emissions according to the latest US Greenhouse Gas Emissions Inventory. For 2021 it was 0.437% and was updated to 0.428% last June 2022.

Xpansiv published in July 2023 its guidance on MPC generation for the Processing, Transmission, and Storage segments. The guidance provides intensity thresholds that operators will have to achieve to generate MPCs.

Xpansiv is a global exchange for ESG commodities, allowing producers and customers to track, measure, and transact commodities based on environmental and other derived attributes. The goal is to enable major commodity groups to operate in a single marketplace so that participants can have a transparent, auditable dataset for registering and claiming ESG attributes tied to specific production units.

Scope 1, 2 and 3

Xpansiv

Fully implemented

2021

Privately funded for-profit

Global

Low cost, moderate effort

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

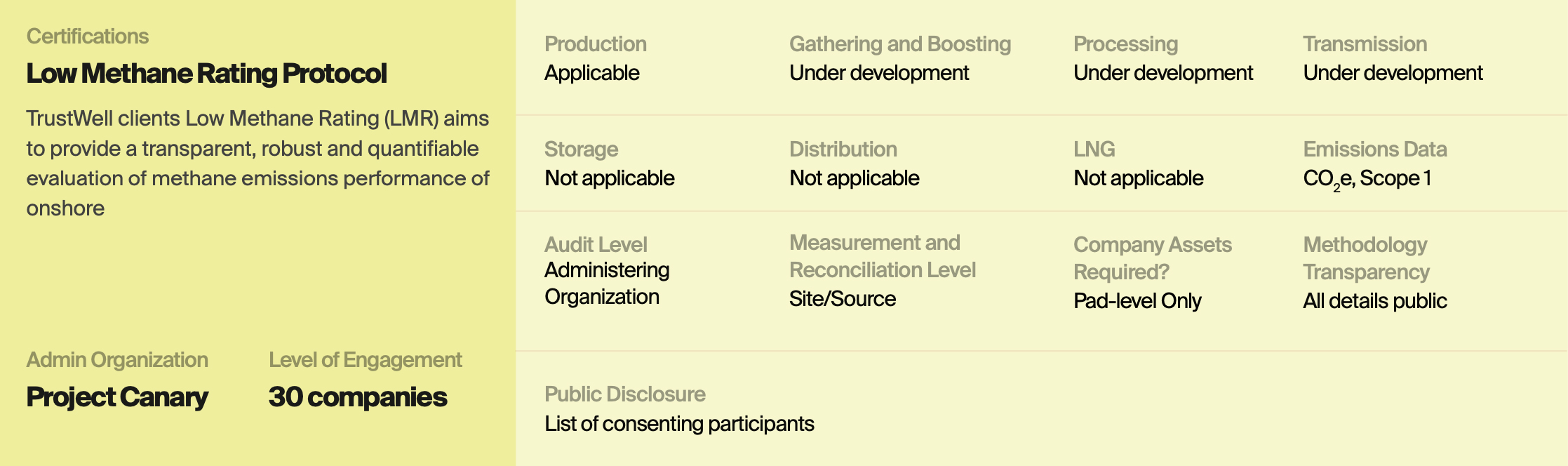

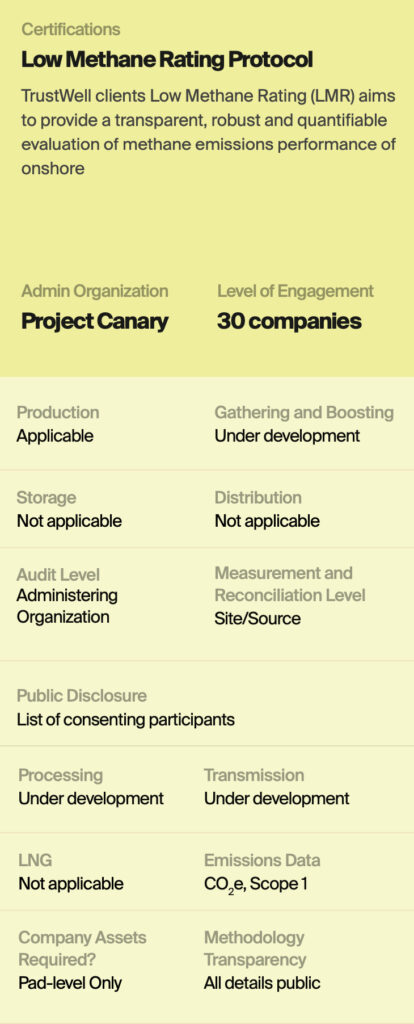

The Low Methane Rating Protocol emphasizes both basin and pad-level methane intensities, eliminating selection bias and providing the most granular level of emissions performance available. The protocol provides differentiation and visibility to operators that are utilizing best industry practices and advanced methane measurement and monitoring technologies.

The comprehensive process provides operators with technology-enhanced registry-ready data that is completely registry agnostic and free of any conflict of interest.

A Low Carbon Rating (LCR) for the midstream sector is currently under development and will be released in 3Q 2023. The LCR will cover the midstream gathering and boosting, processing, and transmission segments.

Project Canary intends LMR to be an evolving and iterative program that adjusts to changes in regulations, industry best practices, and technology landscapes. Multiple stakeholders such as technology providers and consultants will be involved in the program’s continuous improvement.

Scope 1 (Scope 2 and 3 can be included to achieve better ratings)

Project Canary

Fully implemented

2023

Privately funded for-profit

Global

Moderate

Production

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

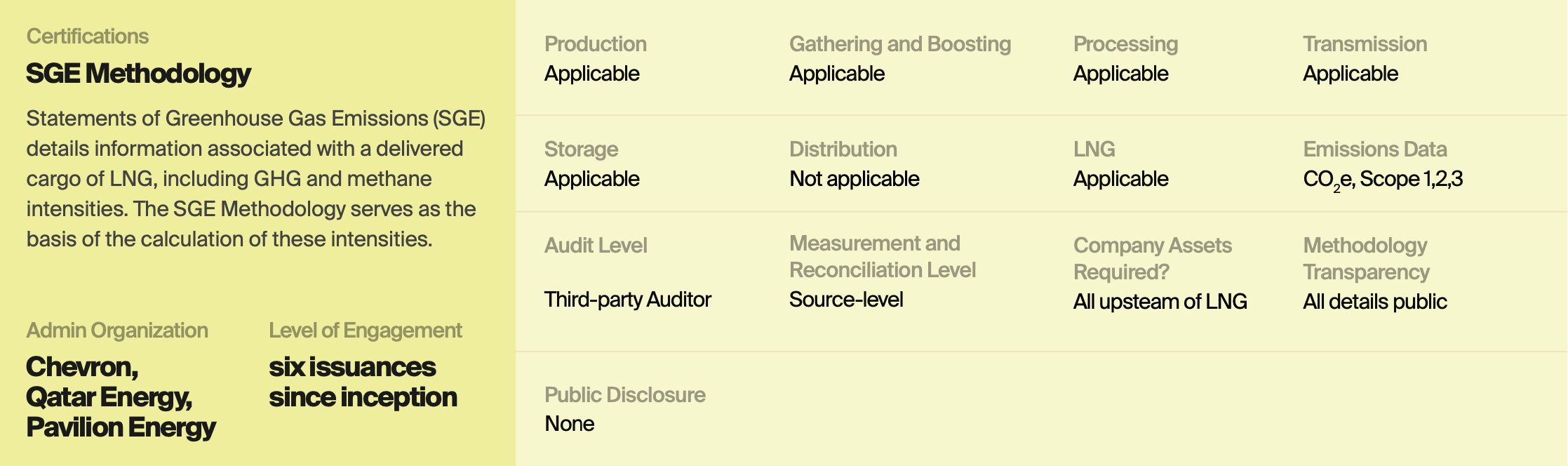

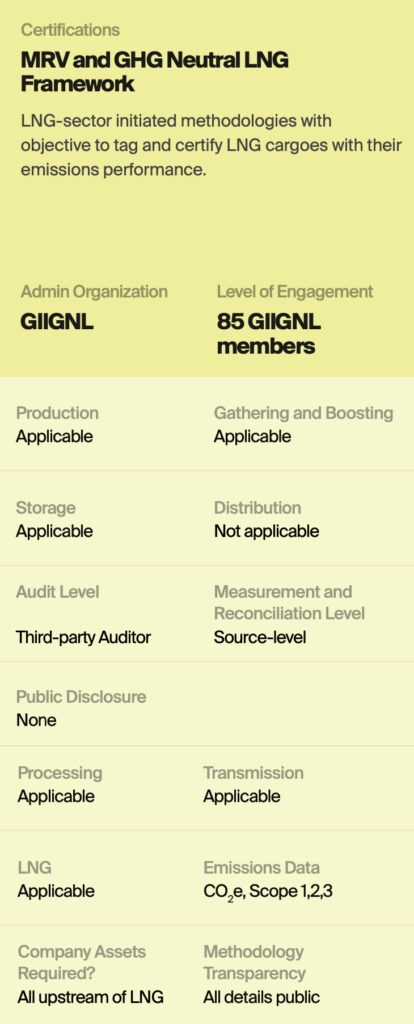

The SGE Methodology establishes a strong foundation for improved emissions accountability throughout the LNG value chain. The emissions associated with a cargo of LNG are quantified, evaluated, and then provided with a Statement of Greenhouse Gas Emissions (SGE) to certify the cargo’s emissions intensity.

The SGE Methodology requires quantification of Scope 1, 2, and 3. Scope 3 emissions quantification is approached based on product life cycle accounting methods from production at the wellhead to delivery at the discharge manifold.

These SGE reports must be done per cargo and require third-party verification to address reasonable assurance expectations.

Unlike SGE Methodology’s similar LNG-sector initiative by GIIGNL, the SGE Methodology explicitly disallows the use of offsets in its cargo tags. Both frameworks, however, agree to the inclusion of the accounting of emissions from carbon capture, utilization, and storage.

The SGE methodology and GIIGNL’s framework establish a strong foundation for improved emissions accountability throughout the LNG value chain, paving the path for additional decarbonization measures toward a lower carbon future from wellhead to burner-tip.

Scope 1, 2 and 3

Chevron, QatarEnergy, Pavilion Energy

Fully implemented

2021

Privately funded for-profit

Global

Moderate

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

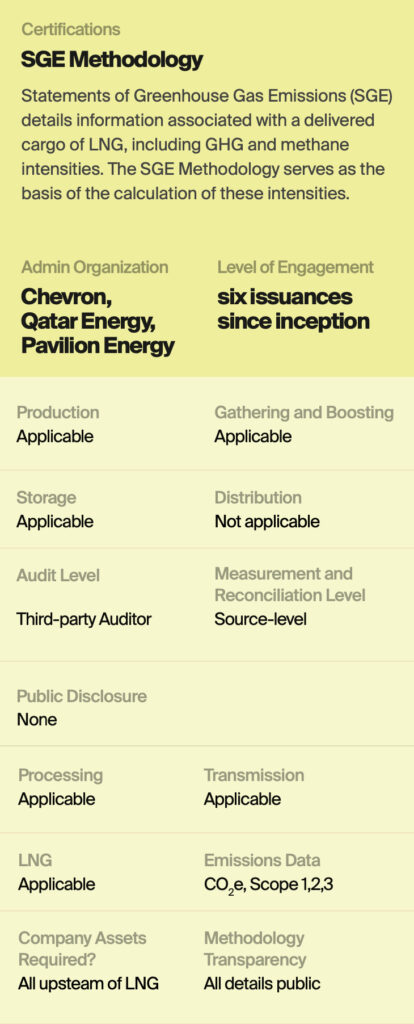

GIIGNL has developed guidelines to quantify the GHG emissions associated with an LNG cargo. These guidelines can be applied either for a specific stage, a partial life cycle, or the entire value chain, including the end-use of the LNG. GIIGNL aims to increase the transparency of emissions accounting in this industry segment by making the Framework accessible to all participants.

For the net overall emissions intensity calculations, the MRV and GHG Neutral LNG Framework allows the accounting of emissions from carbon capture, utilization, and storage. For cargoes using offsets in their quantification for emissions intensity, an “offset-included” cargo statement will be issued instead.”

Aiming to capture the emissions profile of the entire value chain, the framework issues Stage Statements and Cargo Statements. Stage Statements are verified statements of emissions intensity issued to segment participants along the value chain of the specific LNG cargo.

Cargo Statements are verified value-chain GHG profiles of the specific LNG cargo that provide additional information, like whether offsets were used, if there is a robust emission reductions plan, or if the cargo conforms to the carbon neutrality standard specified in the framework.

Scope 1, 2 and 3

Fully implemented

2021

Privately funded for-profit

Global

Moderat

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

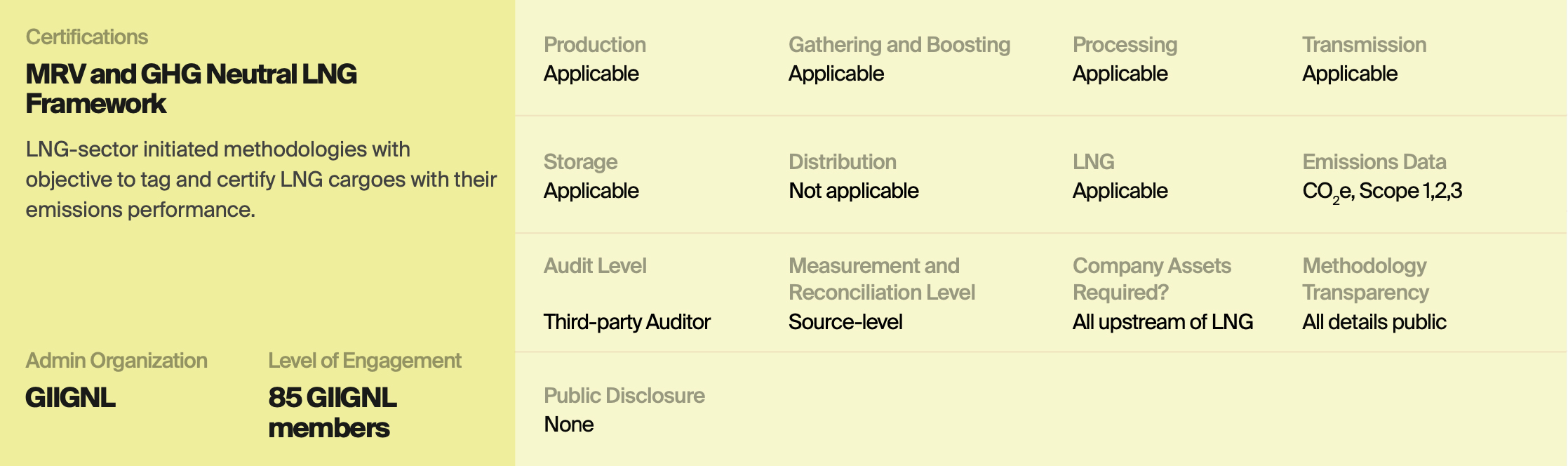

OGMP 2.0 is a comprehensive methane reporting framework for the oil and gas industry, requiring the implementation of measurement-based technologies both at the source-level and site-level. These measurements must be conducted using strict science-based measurement standards.

Participating companies commit to reporting their methane emissions from all operated and non-operated assets across the value chain each year.

OGMP 2.0 provides members a platform to credibly report on methane emissions performance, identify best mitigation options , and engage with and contribute to the leading process for methane management globally.

Company data were collected and analyzed in the second OGMP 2.0 annual report

Approval of additional OGMP 2.0 Technical Guidance Documents outlining source-specific quantification methodologies, including guidance on Uncertainty & Reconciliation

Revision of reporting templates and associated guidance

Scope 1

United Nations Environment Programme

Fully implemented

November 2020

Publicly funded non-profit

Global

Moderate

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

The U.S. Environmental Protection Agency (EPA) Methane Challenge Program is a commitment-driven program that requires participants to transparently report actions towards methane emission reductions every year. Since 2016, the Methane Challenge Program has offered participants two distinct pathways toward emissions reduction, each with its benchmarks and reporting procedures.

The Best Management Practices (BMP) option in the Program is a pathway designed to create a near-term implementation of methane mitigation strategies across the entire oil and gas value chain. Companies will choose at least one emission source appropriate for their industry segment and commit to implementing the best management practice for that specific source across their operations. This commitment includes a five-year timeframe for company-wide implementation. The BMP option also mandates annual reporting procedures to be disclosed to the EPA regarding the rate of progress, key milestones, and context for implementation plans.

Renewable Natural Gas

Equipment Leaks/ Fugitive Emissions Commitment Option for Compressor Isolation and Blowdown Valve Leakage

Participants who join the challenge have access to the benefits of peer networking, information sharing and technology transfer workshop opportunities, and public recognition highlighting individual company achievements.

Scope 1

US Environmental Protection Agency

Fully implemented

2016

Publicly funded non-profit

United States

Low

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

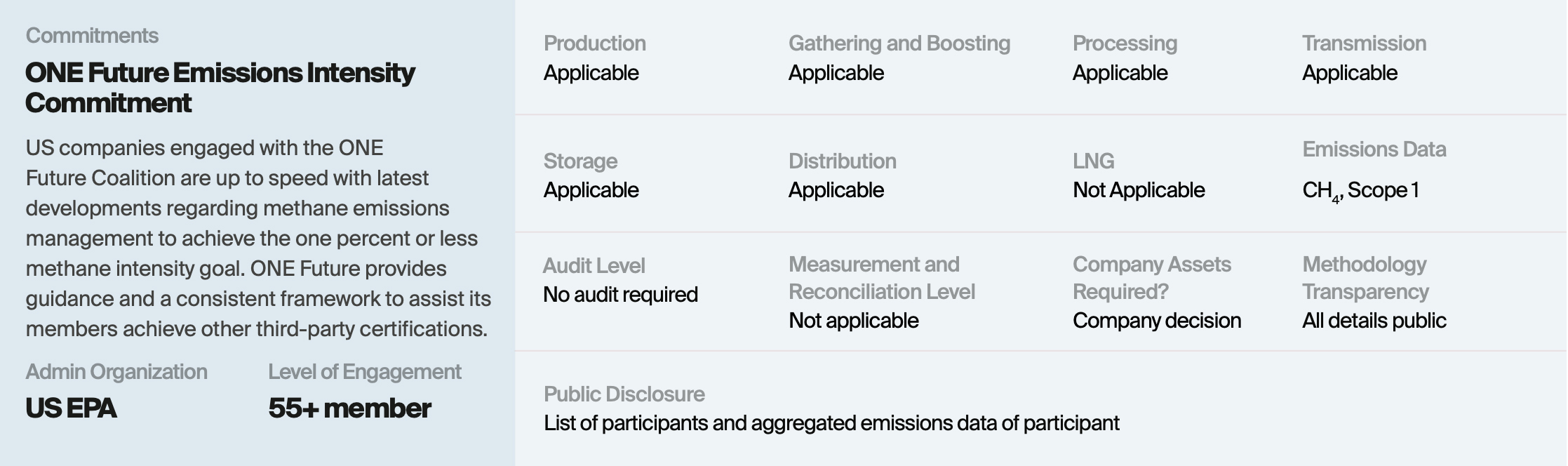

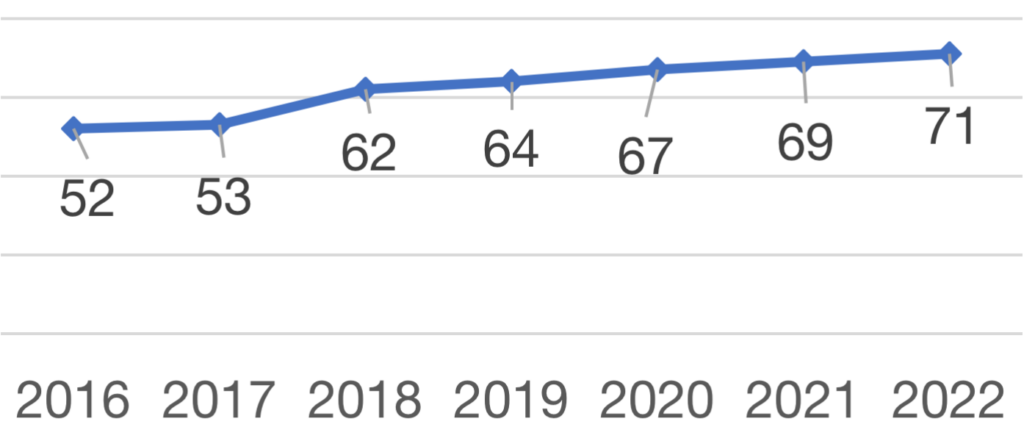

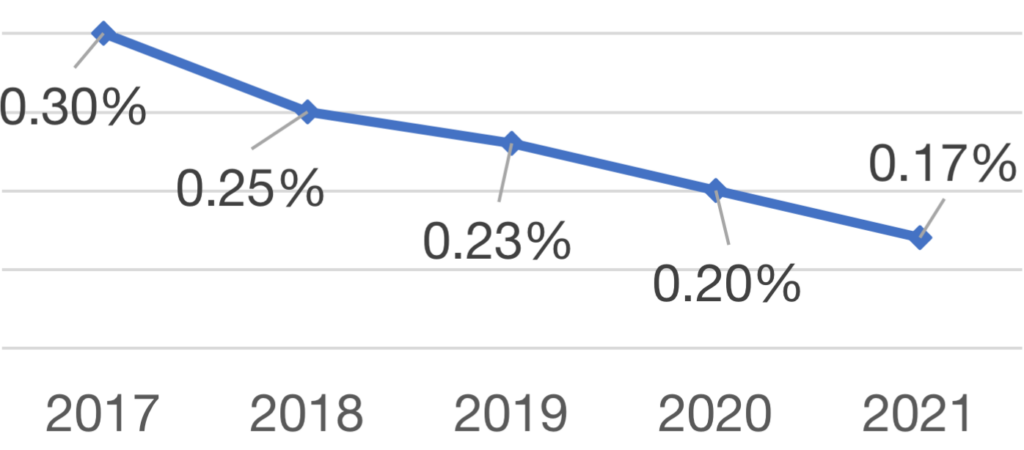

The ONE Future Coalition is a growing group of over 50 U.S. companies committed to voluntarily reducing their collective methane emissions intensity across the natural gas value chain to 1% or less. Founded in 2014, ONE Future has since demonstrated an innovative, performance- and science-based approach to emissions management.

Program participants collectively commit to achieve a methane intensity lower than 1% each year. See their historical progress since 2017 when they set the target:

By joining the coalition, companies commit to reducing emissions in all assets in at least one sector of engagement in the oil and gas value chain. One of the fundamental principles of the ONE Future initiative is allowing participants to allocate capital towards reduction approaches in a way that is tailored to the capacities of each company. Therefore, companies are not mandated to implement any specific technologies or methodologies in their pursuit of emissions reductions.

onefuture.us

Scope 1

ONE Future Coalition

Fully implemented

2014

Privately funded non-profit

USA – Onshore

Low

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

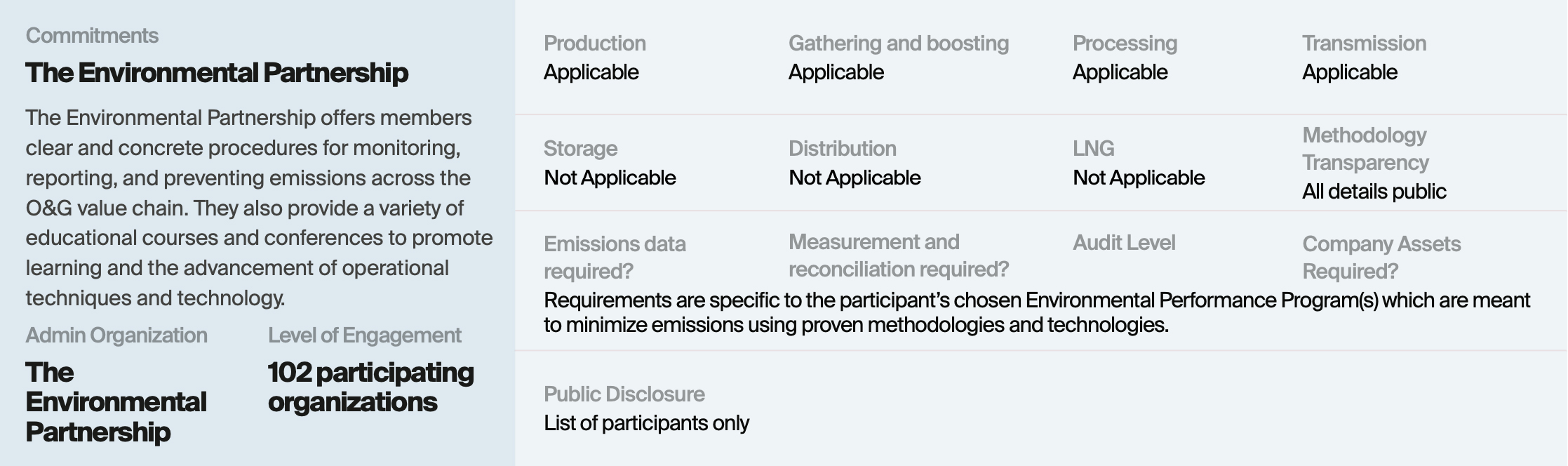

Launched by the American Petroleum Institute in 2017, The Environmental Partnership is an industry-led coalition of oil and natural gas companies that have voluntarily committed to continuously improve the industry’s environmental performance. Through the Partnership, companies are taking action by implementing performance programs within their organizations, learning and sharing best practices and new technologies, and fostering collaboration. Its key value to the industry is providing a platform for operator peer-to-peer sharing across the four critical methane reduction elements of facility design, operations and maintenance, measurement and detection, and data integrity.

Since its inception, the Partnership has quadrupled in industry participants and now represents more than 70% of total U.S. onshore natural gas and oil production, with companies focused on driving innovation and reducing methane emissions in every major U.S. basin.

The Environmental Partnership has created six separate Environmental Performance Programs that operate on various upstream and midstream production components and are meant to minimize emissions.

Since the launch of the flare management program in 2020, The Partnership has advanced best practices to reduce flare volumes, promote the beneficial use of associated gas and improve flare reliability and efficiency when flaring is necessary. Last year, companies participating in the flare management program, who represented 62% and 40% of total U.S. oil and natural gas production respectively, reported an aggregated 45% reduction in flare intensity and a 26% reduction in total flare volumes in 2021 from the previous year.

Since its inception, the Partnership has quadrupled in industry participants and now represents more than 70% of total U.S. onshore natural gas and oil production, with companies focused on driving innovation and reducing methane emissions in every major U.S. basin.

The Environmental Partnership has created six separate Environmental Performance Programs that operate on various upstream and midstream production components and are meant to minimize emissions.

Scope 1

American Petroleum Institute

Fully implemented

2017

Privately funded non-profit

Requirements and methodologies are partially available to the public. Some elements are not disclosed.

Requirements and methodologies are partially available to the public. Some elements are not disclosed.

The Oil and Gas Climate Initiative (OGCI) is a CEO-led commitment by the 12 member companies to reduce their emissions intensities towards near zero. Composed of industry leaders Aramco, bp, Chevron, CNPC, Eni, Equinor, ExxonMobil, Oxy, Petrobras, Repsol, Shell, TotalEnergies, OGCI leverages the capacities of its member companies to accelerate the low carbon transition of the oil and gas industry.

OGCI members are utilizing current detection and quantification technologies, such as the deployment of satellite, aircraft, and drone monitoring, including the deployment of GHGSat capabilities over specific OGCI and non-OGCI assets in regions with limited local capacities, such as in Iraq and in other developing countries.

To support companies outside the group, OGCI focuses on partnering, capacity building and innovations to target key technologies and areas that can have the greatest impact on emissions reductions.

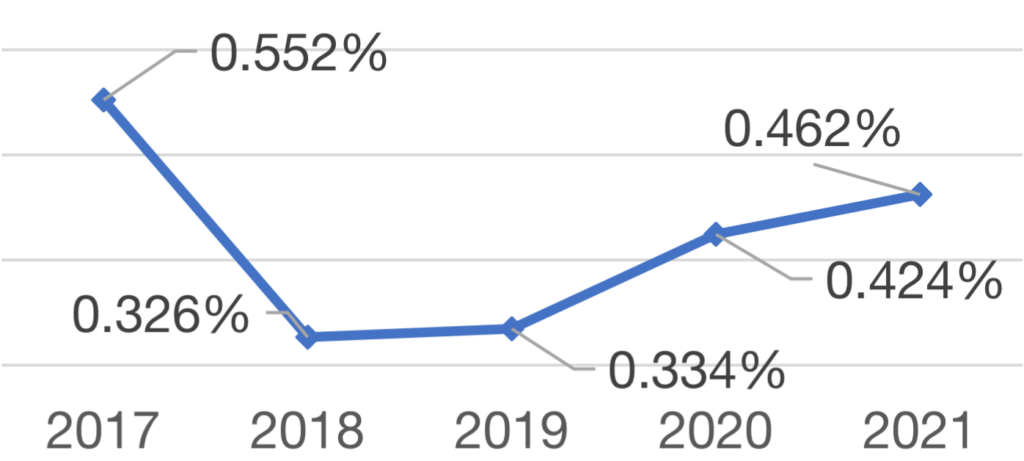

OGCI members commit to achieve a methane intensity well below 0.20% by 2025.

See their historical progress since 2017 when this target was set:

OGCI members are utilizing current detection and quantification technologies, such as the deployment of satellite, aircraft, and drone monitoring, including the deployment of GHGSat capabilities over specific OGCI and non-OGCI assets in regions with limited local capacities, such as in Iraq and in other developing countries.

To support companies outside the group, OGCI focuses on partnering, capacity building and innovations to target key technologies and areas that can have the greatest impact on emissions reductions.

OGCI banks on innovation, stakeholder engagement, and technological competencies as essential factors that will advance the industry towards net zero.

Scope 1, 2, and 3

Oil and Gas Climate Initiative

Fully implemented

2014

Privately funded non-profit

Global

High

Full natural gas value chain, with strong emphasis on exploration and production

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

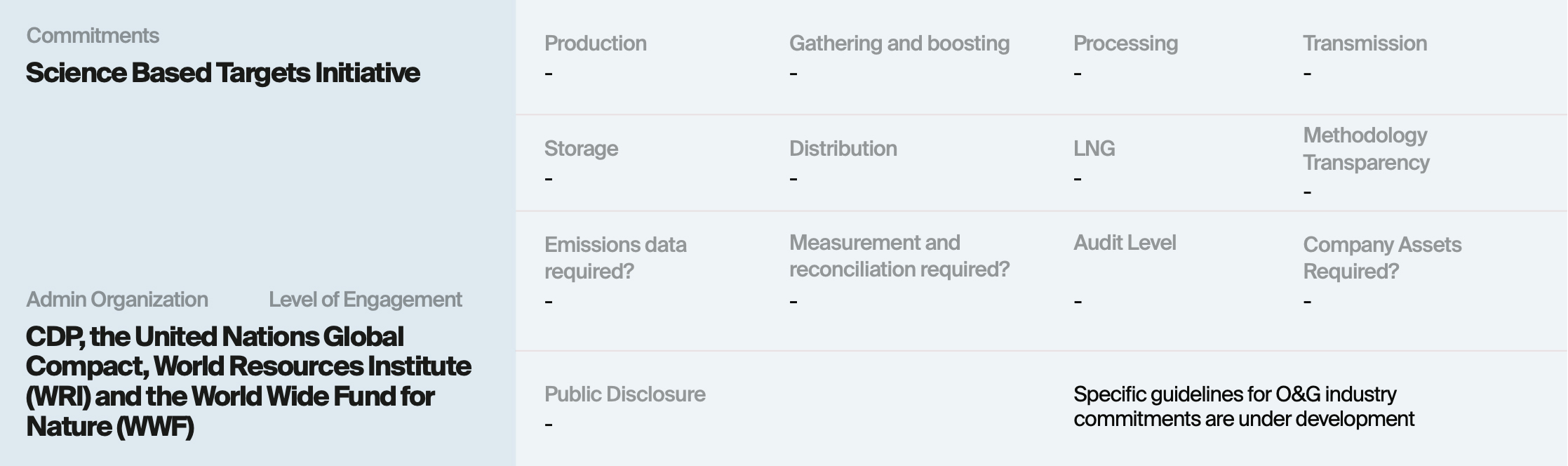

The Science Based Targets Initiative is an emissions reduction program that spans multiple industries in the industrial and commercial landscape, currently with guidance for 13 industries.

The Science Based Targets Initiative (SBTi) was launched in 2015 through a collaborative effort by the UN Global Compact, the World Resources Institute (WRI), the World Wildlife Fund for Nature (WWF), and CDP to support the 1.5°C goals of the Paris Agreement. The SBTi makes companies commit, develop, and communicate action toward a long-term science-based target to reach net-zero value chain emissions by 2050.

The creation of targets considers each company’s unique capacity to reduce its GHG emissions, making it an attractive initiative for SMEs. However, these targets are validated by the SBTi to make sure they are science-backed and aligned with the 1.5°C ambition.

The SBTi is working on its guidance for the oil and gas sector, with the most recent update last January 2023 where SBTi published its Expert Advisory Group Review Evaluation Report.

The Science Based Targets Initiative (SBTi) was launched in 2015 through a collaborative effort by the UN Global Compact, the World Resources Institute (WRI), the World Wildlife Fund for Nature (WWF), and CDP to support the 1.5°C goals of the Paris Agreement. The SBTi makes companies commit, develop, and communicate action toward a long-term science-based target to reach net-zero value chain emissions by 2050.

The creation of targets considers each company’s unique capacity to reduce its GHG emissions, making it an attractive initiative for SMEs. However, these targets are validated by the SBTi to make sure they are science-backed and aligned with the 1.5°C ambition.

TBD for oil and gas sector

CDP, the United Nations Global Compact, World Resources Institute (WRI) and the World Wide Fund for Nature (WWF)

Under development for oil and gas sector

2003

Privately funded non-profit

Global

Low

TBD for oil and gas sector

TBD for oil and gas sector

TBD for oil and gas sector

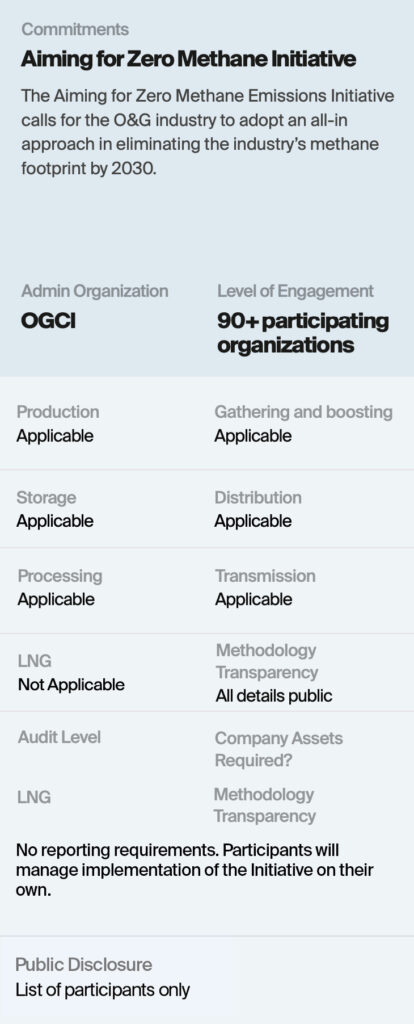

Aiming for Zero Methane Emissions Initiative calls for the oil and gas industry to treat methane emissions as seriously as it treats safety. The goal is to eliminate the industry’s methane footprint by 2030.

Aiming for Zero does not mandate specific guidelines or methodologies for reporting methane emissions. It is meant to complement existing multi-stakeholder voluntary initiatives such as OGMP 2.0 and the Global Methane Pledge.

Companies involved in oil and gas exploration, extraction or production can be signatories; other organizations can join the initiative as supporters. Signatories of the initiative strive to meet the near-zero methane emissions goal and are ready to disclose GHG emissions or metrics. Supporters also endorse the initiative and encourage new participants to join.

Since its inception in June 2022, the initiative has garnered over 90 signatories and supporter

The initiative’s secretariat is currently hosted by OGCI, with the intent of transferring control to another international organization in the short- to mid-term. OGCI has published its near-zero methane emissions guidance in August 2023.

Companies involved in oil and gas exploration, extraction or production can be signatories; other organizations can join the initiative as supporters. Signatories of the initiative strive to meet the near-zero methane emissions goal and are ready to disclose GHG emissions or metrics. Supporters also endorse the initiative and encourage new participants to join.

Since its inception in June 2022, the initiative has garnered over 90 signatories and supporter

Aiming for Zero is designed to supplement existing multistakeholder initiatives such as Methane Guiding Principles and IPIECA, and therefore does not have its own specific methodologies.

Scope 1, 2 and 3

Oil and Gas Climate Initiative

Fully implemented

2022

Privately funded non-profit

Global

Low

Full oil and gas value chain

TBD for oil and gas sector

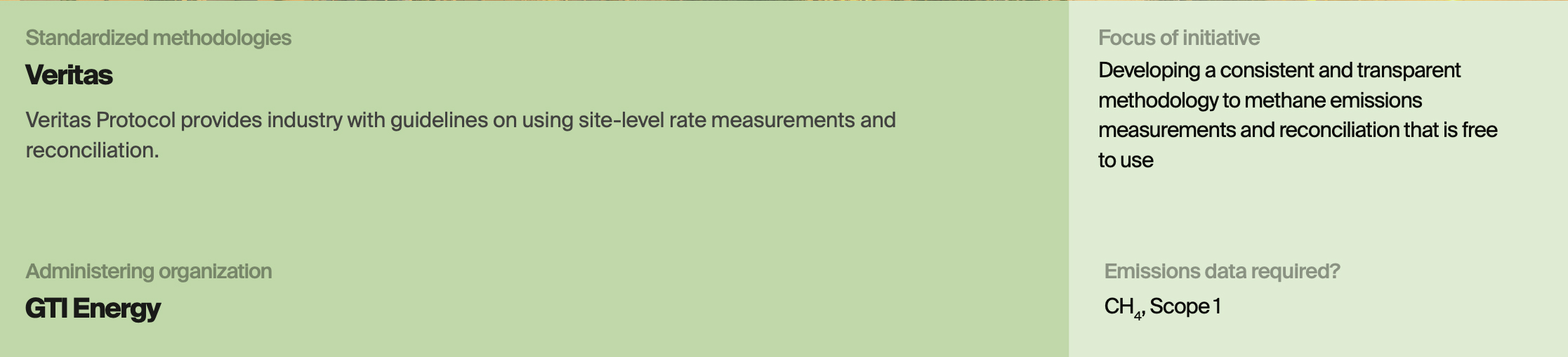

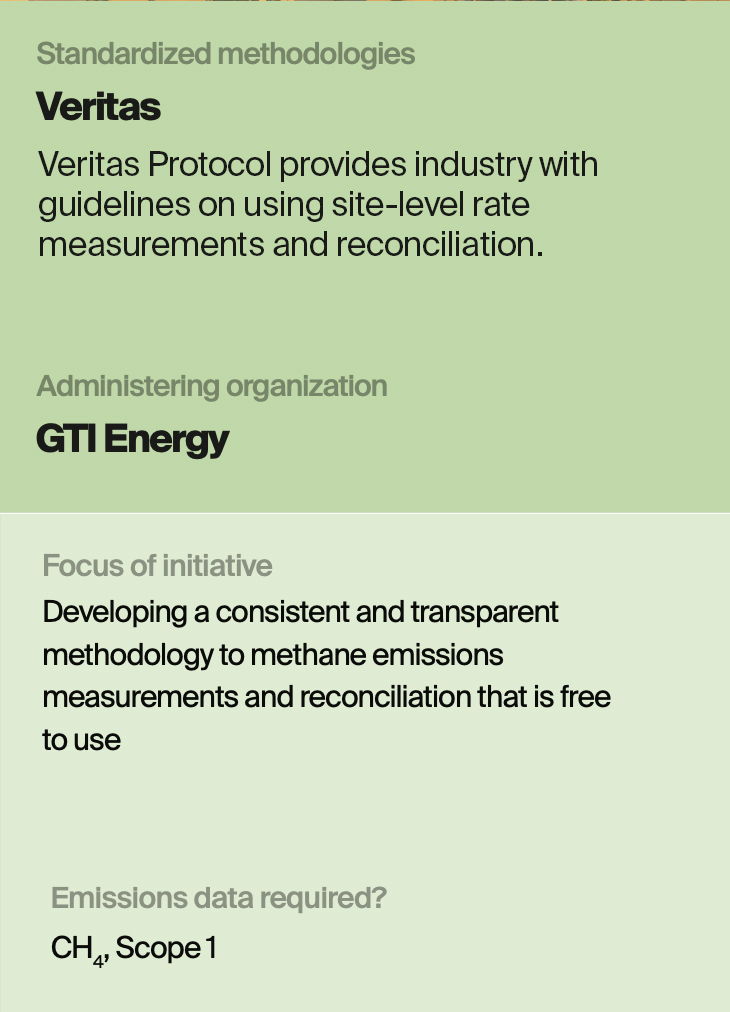

GTI Energy’s Veritas initiative provides a standardized methodology for calculating and reporting methane emissions across all segments of the natural gas supply chain. The technical methodologies allow companies and countries to adopt a consistent approach in setting methane emissions reduction targets, as well as measuring and verifying reported methane emissions.

By publishing these protocols, the Veritas initiative aims to guide the oil and gas industry in building measurement-informed methane inventories that are comparable across different companies in the same supply chain segment (e.g., production).

Currently, Veritas covers only methane emission sources in the natural gas industry.

GTI Energy plans to release Version 2 of the Veritas protocol in December 2023.

Additional funds raised and workstream to develop source-based methane emissions measurement to facilitate alignment with other methane emissions initiatives (such as OGMP 2.0).

There are plans to expand the scope to include other sources including landfill and agriculture.

Scope 1

GTI Energy

Fully implemented – protocols released publicly February 2023

2022

Privately funded non-profit

North America

Moderate

Applicable to all oil and gas industry segments

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

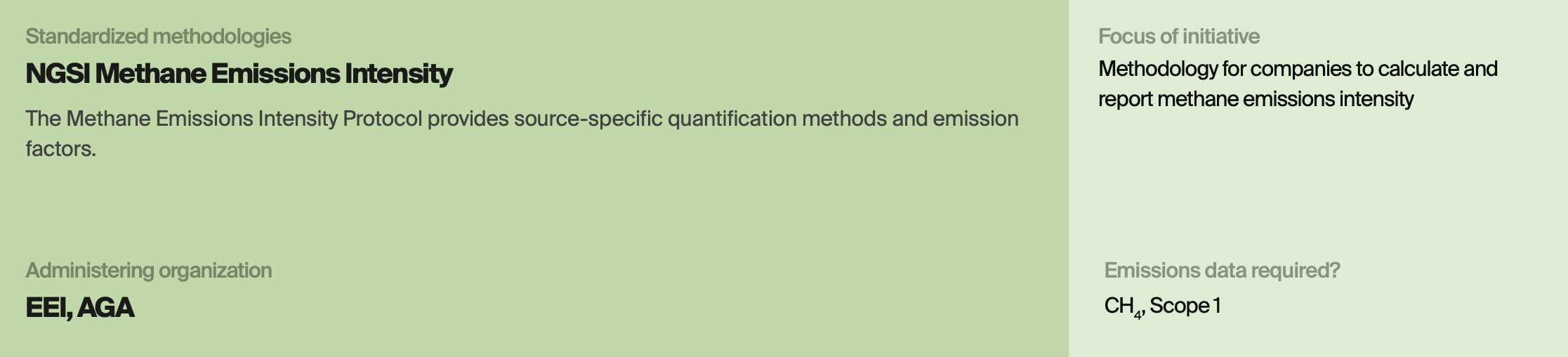

The Natural Gas Sustainability Initiative (NGSI) is an industry-led effort to address ESG issues throughout the natural gas supply chain. NGSI aims to provide an openly available monitoring and reporting framework that specifically tackles methane intensity.

The Methane Emissions Intensity Protocol Version 1.0 is the main resource offered by the NGSI. The protocol is a detailed calculation and reporting methodology that builds on existing approaches to examining methane intensity, and it incorporates emissions that may not meet the intensity thresholds of other reporting schemes.

Since its inception, the NGSI Protocol has been widely adopted by other initiatives for their quantification methods.

The NGSI has expressed plans to include direct measurement in future versions of the protocol. The protocol is non-prescriptive regarding the deployment of monitoring technologies. Accountability among NGSI participants may be assured through adherence to their reporting procedure.

Scope 1

Edison Electric Institute (EEI), American Gas Association (AGA)

Fully implemented

2021

Privately funded non-profit

USA – Onshore

Low

All initiative requirements and methodologies are fully transparent and publicly available. All calculations, methodologies, and scoring criteria are clearly defined.

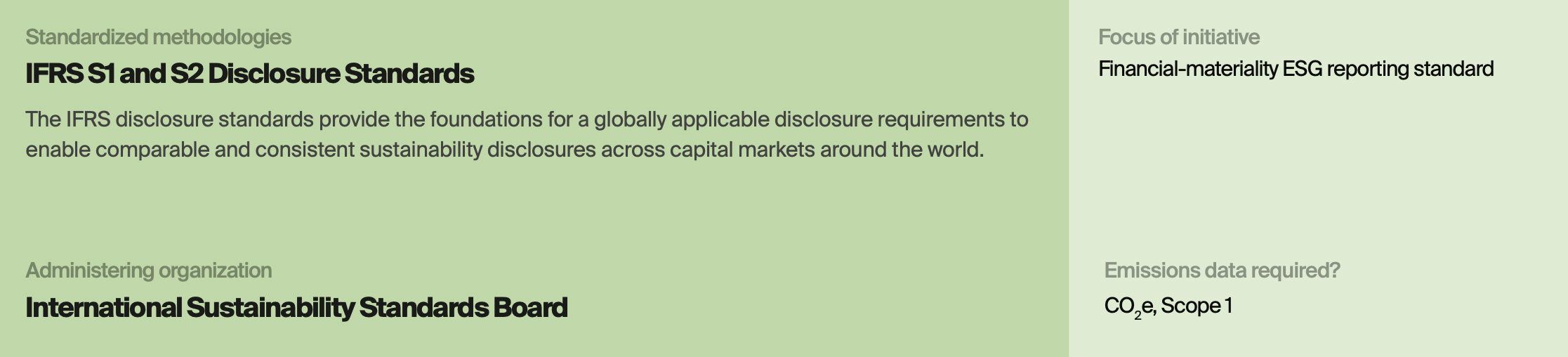

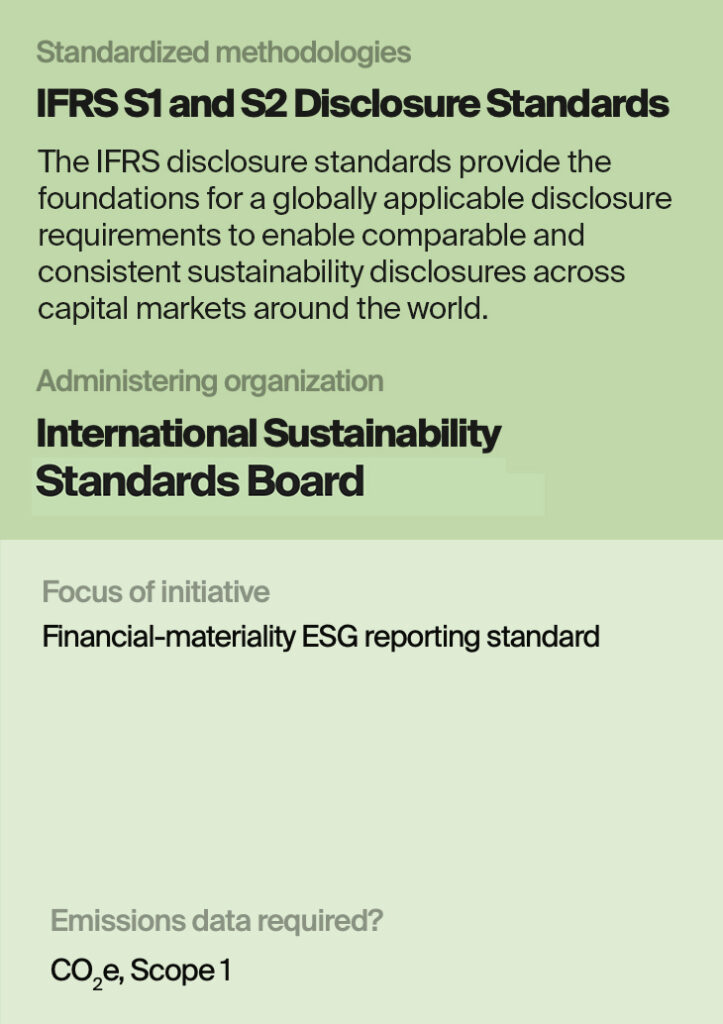

IFRS S1 and S2 Disclosure Standards is a new investor-focused sustainability disclosure standards that is built off of the TCFD Recommendations and the SASB Standards.

The launch of the IFRS S1 and S2 marks an important milestone towards consolidation and harmonization of initiatives.

ISSB also recognizes the complementary nature of using the IFRS S1 and S2 Disclosure Standards with the GRI Oil and Gas Sector Standard to provide a comprehensive and holistic disclosure that caters to both stakeholders and investors.

As of July 25, 2023, the International Organization of Securities Commissions (IOSCO) has formally endorsed the IFRS S1 and S2 Standards as an effective global framework of investor-focused disclosures in relation to climate-related matters (IFRS S2) and, more generally, sustainability-related information (IFRS S1).

Scope 1 and 2

International Sustainability Standards Board (ISSB)

Fully implemented

2023

Publicly funded non-profit

Global

Low

Exploration and production, midstream, refining and marketing, and oil and gas services